New scale requirements for DC master trusts: transition pathway and credible growth plans

On this page:

- Purpose of this statement and key points

- Background

- Market impacts

- Preparing for scale

- Credible growth plans: principles

- Quantifying the path to scale

- Next steps

- Annex: assumptions used in our analysis

Purpose of this statement and key points

The Pension Schemes Bill (the Bill) will introduce important new duties for defined contribution (DC) master trusts to meet certain size requirements. The Bill is currently progressing through Parliament and more detail will follow in secondary legislation, codes and guidance over the coming months and years.

The announcement of the new scale requirements has already had a significant impact on the commercial DC master trust market, with corporate activity increasing as a result. The behaviour of market participants such as employers and employee benefit consultants (EBCs) has also been affected, with perceived risks around scale informing employer selection and deselection of master trusts. We are aware of the potential impacts this may have on savers.

To help address some of these issues, the Department for Work and Pensions (DWP) has published Pension Schemes Bill – Scale and Consolidation explaining the policy intent and principles underpinning the new scale requirements.

This statement complements the DWP’s policy document and aims to provide further detail in the interim period to support master trusts and other parties preparing for these coming changes and aid understanding of what the requirements mean for automatic enrolment (AE) compliance. The statement:

- sets out our early thinking on the principles on which a scheme seeking to enter the transition pathway in the future might base a credible plan to get to scale

- includes some analysis of indicative growth scenarios and key drivers based on a range of assumptions to help inform those assessing the ability of existing master trusts to grow to scale in the applicable timescales and to support conversations about scheme selection

While not every master trust will achieve scale of £25 billion by 2030 or 2035, employers and their advisers should not assume that all master trusts not yet at scale will be unable to meet the criteria. Our supporting analysis suggests there remains significant momentum and growth potential in the master trust sector as a whole. We have included some indicative scenarios below to illustrate how growth may be achieved. Selection decisions should be based on an objective appraisal of the value offered by the scheme and other relevant factors affecting potential saver outcomes.

Published: 9 March 2026

Background

The government’s stated aim for the scale reforms introduced by the Bill is to drive consolidation among DC master trusts and group personal pensions (GPPs), guiding the market to one with fewer, larger schemes that deliver value for savers and can invest more effectively in the UK economy.

In particular, for a scheme to be approved for AE purposes, GPPs and master trusts will need to have at least one main scale default arrangement (MSDA) of at least £25 billion in assets under management (AUM) by 2030. These requirements will start no earlier than 1 January 2030, with some limited exemptions set out in future secondary legislation.

The Bill also introduces a transition pathway to allow additional time for smaller schemes to reach scale by 2035. The detail of how this pathway will operate will be set out in regulations. If a master trust or GPP can demonstrate that it will have at least £10 billion in AUM in a MSDA by 2030, it can apply for transition pathway relief and submit a credible plan to the relevant regulator on how it will grow to at least £25 billion in AUM by 2035. Other conditions will apply and will be detailed in future regulations.

The Bill will deliver a package of interconnected measures across the DC market. Master trusts will also have to consider other requirements, such as demonstrating sufficient investment capability (a new master trust authorisation criterion), undertaking annual value for money assessments, and offering a default guided retirement product.

This statement is high-level and subject to future regulations and accompanying documents. At this stage it is intended to support the industry early on with considerations that are relevant now.

Market impacts

Based on insights from our engagement with the market, we understand that it is already being influenced by the scale policy ahead of the new duties coming into force. For example, some smaller master trusts indicated that they are being excluded from EBCs’ selection lists for prospective employers because of assumptions about their ability to qualify for the transition pathway by 2030 and meet scale by 2035.

While consolidation with a better-performing or better-managed scheme can be in the interests of members, consolidation is not without costs. We are therefore keen to ensure that members do not suffer unnecessary upheaval and increased costs due to the market over-estimating the risk of a scheme not meeting the scale requirements.

As suggested in our analysis below, it is quite possible for a smaller master trust to reach scale over the next 10 years. We are therefore sharing some insights into the key factors contributing to growth and what we will look for in credible plans from master trusts when approving them for transition pathway relief in the future. This is to help schemes prepare for the forthcoming requirements, to support informed discussions among stakeholders, and for parties to be able to fully assess the options available to ensure compliance with AE obligations, once the scale requirements take effect.

Preparing for scale

Trustees of master trusts should start preparing for the significant changes ahead (including scale, value for money, small pots consolidation and guided retirement) and what these mean for their scheme, and consider what’s best for members in line with their fiduciary duties.

Developing a growth plan and analysis that demonstrates the potential of the scheme to reach scale as part of wider business plans will help identify next steps and support conversations with other parties on what the scheme can offer.

Employers and their advisers also play a critical role. Their decisions have a significant impact on the structure of the market and the outcomes for savers. When selecting or reviewing a master trust, we expect employers and advisers to consider a range of factors and their impact on members, such as the following:

- Compliance with AE requirements.

- Value for money, assessing investment outcomes and strategies along with the level of services that the scheme provides relative to costs and charges.

- The quality of governance and of the scheme’s systems and processes.

- Readiness for compliance with future requirements under the Bill, including scale and credible growth plans.

- Administrative and transition processes.

There is a long lead time before regulations are finalised, transition pathway approval begins (expected in 2029), and the scale requirements start (2030). We will continue working with the DWP, the Financial Conduct Authority (FCA), master trusts and industry to support the development of regulations and schemes’ readiness, and to develop further communications, codes and guidance where necessary.

Credible growth plans: principles

Subject to the Bill obtaining Royal Assent, the government will work with us and the FCA to develop and consult on draft regulations and continue engaging with industry throughout. We will also work with government to create supporting guidance on how master trusts can demonstrate a credible plan to grow to scale and meet other conditions for transition pathway relief when the application process is switched on in 2029. The considerations set out below are intended as a framework to support master trusts in developing their plans and positioning their growth potential to the market now.

Growth plans should cover both the non-financial aspects of the scheme – like governance, operational resilience, and capability – and financial aspects, as outlined below.

We do not expect master trusts to submit a revised business plan outside their annual submission cycle for us to assess their credibility. Instead, they will likely need to provide a clear, actionable roadmap document with key delivery milestones and strategies to achieve them. These plans should focus on growth forecasts underpinned by a range of appropriate assumptions and supported by robust evidence. We will review this information alongside existing data and our knowledge of each master trust.

Growth forecasts

Plans will have to show how the master trust will grow from its current position to:

- at least £10 billion in AUM in their MSDA by 2030

- at least £25 billion in AUM in their MSDA by 2035

The plan will likely include the projected AUM in a scheme’s MSDA starting from the baseline, with forecasts based on assumptions around the following key categories:

- Organic growth: Growth achieved through existing operations and relationships, rather than transactions such as mergers and acquisitions. It includes increases in contribution levels, strategies to increase member retention rates, employer acquisition strategy, and is influenced by competitiveness of the scheme’s charging structure, value for money, and customer satisfaction.

- Demographic and economic factors: Based on official forecasts on key factors including wage inflation, employment rates, and population size.

- Investment returns: Linked to past performance and short-to-medium term market forecasts.

- Inorganic growth: Growth through external transactions, as opposed to the internal expansion covered above under organic growth. It can include scheme consolidation through taking on non-workplace DC schemes, mergers or acquisitions to combine with another master trust, or strategic alliances with complementary organisations to accelerate growth.

For each category, the master trust will likely need to specify the relevant metric and set out the approach taken to develop robust assumptions, including the evidence of the assumptions underpinning them. They may also want to show what steps they have already taken to progress towards scale. The level of detail should be proportionate and reflect the scheme’s starting level relative to the £25 billion target.

Forecasts should be credible, using realistic assumptions. For material elements, schemes may include low, mid, and high scenarios. However, low and high scenarios are provided solely to illustrate sensitivity and potential variability and we would not expect them to be included in the growth forecasts.

Inorganic growth assumptions

By their nature, inorganic growth assumptions are harder to evidence and therefore need detailed consideration of the factors that affect success. The effectiveness of an inorganic growth strategy will be influenced by financial and non-financial considerations including the following:

- Clarity of mission, objectives, and value proposition.

- Scheme and scheme funder / corporate group infrastructure, including:

- experience of management and operational team, and clear support backing on strategic direction from the executive board and owners

- capacity and scalability of the offering, platforms, systems and administrator capabilities

- available funding sources, including existing cash reserves and viable financing options

- Track record of recent financial performance, previous consolidations, and new business wins.

- Robustness of assumptions.

If a master trust intends to include inorganic growth that contributes a vital element to its AUM projections, we expect there to be an objective assessment based on the above criteria. We anticipate this assessment would be underpinned by proportionate market analysis, incorporating relevant data, and clearly demonstrate an understanding of the scheme’s position within its market and strength of that position. Assumptions must be realistic and reflect the size of the opportunity and likely success rate.

Quantifying the path to scale

Contributory growth factors

As discussed above, a scheme’s future trajectory is based on a number of variables that can contribute significantly to growth. These include the following.

Organic factors

- Net contribution flows from existing employers / members.

- Wage inflation.

- Investment returns.

- Inflows from new employers and single employer schemes.

Non-organic factors

- Mergers, acquisitions and other corporate activity.

- Bulk transfers from non-workplace sources.

To demonstrate how these can impact on a scheme’s ability to achieve scale, we have developed high, medium and low assumptions for each of the 'organic' factors above (further details of these assumptions are given in the Annex). These have been combined into three potential growth scenarios, each expressed in the form of an indicative compound annual growth rate for the 10 years to 2035:

Table: Growth scenarios

| Scenario | Compound annual growth rate (CAGR) 2025 to 2035 |

|---|---|

| High | 16.9% |

| Mid | 12.3% |

| Low | 8.0% |

To add some historical context to these potential scenarios, the total AUM of the trust-based DC workplace market (excluding micro and hybrid schemes) grew by a compound annual growth rate of 22.4% over the 10 years to 2024, albeit from a lower base.

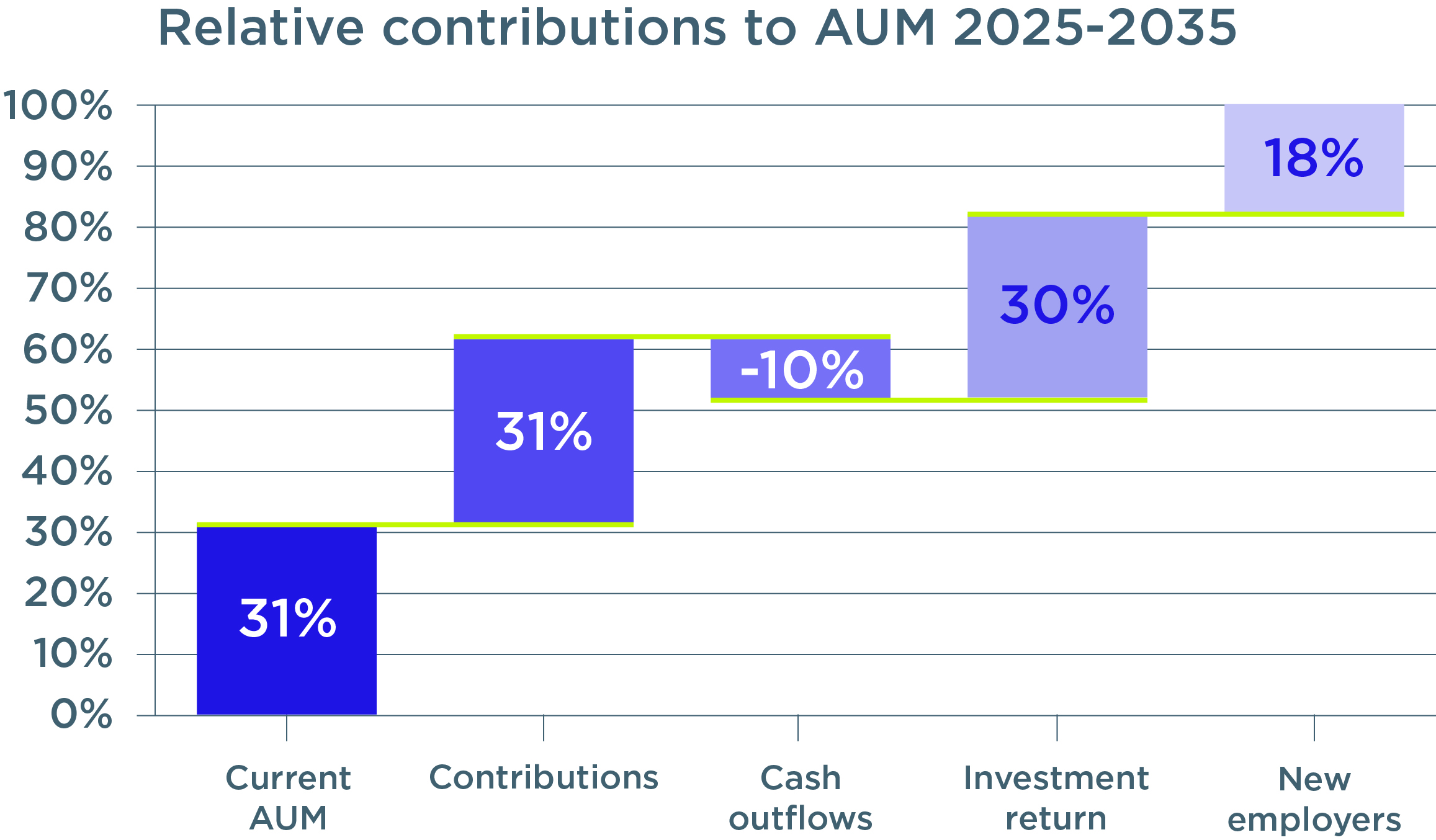

As an illustration of the relative impact of each of the factors, the contributions to growth within the mid-range scenario above are displayed in the following chart:

As this shows, we might expect the majority of the growth in assets to be driven by the compounding of current AUM with ongoing contributions from existing employers and investment returns. The contribution from new employers to the scheme would be expected to have a lower impact on overall scheme growth.

In practice, these factors and their relative impacts will differ from scheme to scheme. The use of assumptions here is for indicative purposes only, and these scenarios should not be relied upon as evidence that any scheme will or will not achieve the required level of scale within the prescribed timeframe. Our projections are intended to give a broad indication of the potential for future growth. Whilst they include assumptions for organic new business growth, such as from new employers joining the scheme, they do not reflect the potential impact of non-organic growth, such as scheme mergers or acquisitions.

Next steps

We will continue to monitor market developments and engage with industry as the policy and detailed legislation develops. We encourage stakeholders to engage with us on any issues arising from the forthcoming requirements that are likely to affect them and we will provide further communications as appropriate.

Annex: assumptions used in our analysis

Net contribution flows from existing employers/members

For the purposes of this analysis, we are using fixed assumptions for net contribution flows. These are based on the following:

- Average contribution rates calculated from the entire UK DC market.

- Outward cash flows starting from current levels and increasing on a linear path towards an assumed steady state of 3.5% per annum of AUM by 2045.

- No other allowance has been made for transfers out, full annuitisation, death benefits or other cash flows out of the scheme.

Wage inflation

The rate of growth in average regular wages from January 2000 to October 2025 was 3.4% per annum, while the CPI measure of inflation was 2.6% per annum. Assuming that future inflation will be closer to the Bank of England’s inflation target of 2%, we are using a mid-point projection of 3% per annum with a range of 2% to 4% per annum.

Investment returns

Current investment return forecasts used by master trusts in their business plans generally fall within the range of 5% to 8% per annum. This reflects that a majority of money currently within master trusts is invested in the growth phase of the member journey, where expected returns are at their highest. As schemes mature in the coming years, we expect they will hold a greater proportion of lower risk investments as the weight of members in the pre- and post-retirement phases increases.

For our illustration here, and with reference to publicly available capital market assumptions, we have assumed a mid-point investment return of 5% per annum, with a range of 3% to 7% per annum. However, this is based around long-term (eg 10-year) assumptions, and significant market volatility can often occur over shorter periods. The journey to scale includes some shorter-term milestones, such as the requirement to have at least £10 billion in the main scale default arrangement by 2030, and schemes should consider the impact of short-term volatility on their position.

Net new business

Net new business flows will vary significantly between schemes and can include both 'organic' growth from ongoing contributions, new employers and single employer DC schemes and 'inorganic' growth from acquisitions and mergers, new strategic partnerships or consolidation from non-workplace sources. The assumptions here relate only to the organic element of these flows.

Significant consolidation from single-employer schemes into master trusts has already taken place, with the total number of occupational DC schemes (including hybrids but excluding micro schemes) falling by 75% over the 13 years to 2024. Nevertheless, there is still substantial consolidation activity under way and consideration should also be given to the potential for transfers from contract-based arrangements, once contractual override rules are in place. For the purpose of this analysis, we have assumed a mid-point level for net new business of 3% of AUM per annum within a range of 0% to 6% per annum.

Note that as the scale requirement relates to the MSDA rather than the total scheme AUM, schemes with a high proportion of members in self-select options will need a correspondingly higher level of assets.