A review of defined benefit (DB) pension schemes with valuation dates between September 2020 and September 2021 (Tranche 16).

Published: 24 June 2021

Introduction

This analysis of the expected positions of defined benefit (DB) pension schemes with valuation dates between 22 September 2020 and 21 September 2021 (Tranche 16) gives further context to our 2021 Annual Funding Statement (AFS) but does not supersede it. The analysis is necessarily technical in nature and so is primarily aimed at a more technical audience than the main 2021 AFS.

In modelling the impacts of market conditions on schemes, we have made a number of approximations based on the high level and limited data we hold, which means we cannot take account of all scheme-specific characteristics. The method and simplifications we have made are contained in the methods, principal assumptions and limitations appendix. The position of individual schemes will vary depending on a number of individual factors, not considered here.

The strength of the employer covenant is a key consideration for trustees and employers when setting their funding strategies. In previous years’ analyses, with the exception of last year, we have shown trends in potential employer affordability. This analysis was based on historic, publicly available information on profit, shareholder funds and dividend payments. Given the significant and uneven impact of the COVID-19 crisis on scheme employers, for many schemes, recent trends in employer affordability based on historic data are likely to be of limited use in assessing employer affordability today. Consequently, we have again excluded trends in employer affordability from this year’s analysis. We have also again excluded data showing segmentation of Tranche 16 schemes into the AFS categories (A-E) as this data is also based on historic assessments of employer covenant.

The remaining analysis is similar to the analysis carried out in previous years.

This material and the work involved in preparing it are within the scope of and comply with the Financial Reporting Council’s Technical Actuarial Standard 100. For the purpose of this standard, the users of this material are considered to be the regulated community of UK occupational DB pension schemes.

Summary

Market conditions and impacts on scheme funding levels

Our analysis shows that most major asset classes invested in by UK pension funds achieved substantially positive returns over the three years to 31 December 2020 and the three years to 31 March 2021.

For example, over the period from December 2017 to December 2020, the FTSE All World (excluding UK) Index returned +36% in sterling terms, and for the period March 2018 to March 2021 the return was +47%. The return on FTSE British Government fixed over 15 years index was +28% over the three years to December 2020, and +10% over the three years to March 2021 (see table 1).

Nominal gilt yields were significantly lower at 31 December 2020 than they were three years earlier, whereas at 31 March 2021 nominal gilt yields were lower than they were three years ago but not to the same extent. Real yields at all durations were much lower at 31 December 2020 than they were three years earlier, whereas at 31 March 2021 real yields were much lower at short durations, similar at medium durations and slightly higher at longer durations than they were three years earlier (see Figures 1 and 2).

For the purpose of this analysis as at 31 December 2020 we have assumed the liabilities are calculated using discount rates which have the same margin over gilt yields that they had at a scheme’s last valuation date. For the analysis as at 31 March 2021, we have assumed that liabilities are calculated using discount rates which have a 0.1% per annum lower margin over gilt yields than was used at a scheme’s last valuation date. We have also made an allowance for the alignment of RPI to CPIH from 2030. Based on the average maturity of the universe of schemes and the expectation that the current RPI curve factors in the change from 2030, we have assumed that the gap between RPI and CPI will be 0.05% lower than at the previous valuation. Together with the change in gilt yields this means the technical provisions (TPs) are likely to have grown over the three years to 31 December 2020 and 31 March 2021, respectively. For the purpose of this analysis, we have not attempted to quantify the potential impact of COVID-19 on schemes’ mortality experience or assumptions. Nor have we considered what, if any, adjustment is appropriate to apply to the CMI 2020 projections.

In practice, the COVID-19 crisis may have impacted the strength of the employers’ covenant which should be reflected in the TPs. This has not been reflected in our analysis.

Overall, our modelling also suggests that schemes undertaking valuations at 31 December 2020 will show similar funding levels but slightly worse deficits from those reported three years previously and the current recovery plan (RP) will not be on track to remove the deficit by the end date. Schemes undertaking valuations at 31 March 2021 will have improved funding levels and deficits compared to those reported three years previously. See Figures 5a and 5b.

However, the position for individual schemes will vary greatly compared with our aggregate estimates. This variation will depend on scheme-specific inter-valuation experience, valuation dates, funding assumptions and investment strategies. For example, at 31 December 2020 schemes that had materially hedged interest rate and inflation risks appeared to have slightly improved funding levels compared to three years previous while unhedged schemes were behind targets. This variation in funding level is demonstrated in Figures 7a and 7b.

Implications for recovery plans (RPs) and affordability

Our modelling shows that if Tranche 16 schemes all had 31 March 2021 valuation dates and were to retain their RP end dates, or for those schemes nearing the end of their RP make a modest increase in the RP length (to bring the length to three years), the median required increase in deficit repair contributions (DRCs) for those schemes still in deficit would be around 0% to 25% (see Figure 8). 34% of schemes would be able to retain their DRCs at the same level or less, while just 4% would need to increase DRCs to more than three times their current level. Some of this latter group of schemes would need to increase DRCs by much more than this.

As mentioned above, in practice, the COVID-19 crisis may have impacted the strength of the employers’ covenant which should be reflected in the TPs. This has not been reflected in our analysis. Strengthening of TPs will increase the deficit and, if the RP end date is to be maintained, will lead to higher DRCs than our analysis shows.

In addition, DRCs may be limited by employer affordability, especially in the short term where employers have been materially impacted by COVID-19.

Market indicators

Scheme funding is sensitive to the impact of the changes in market conditions on schemes’ assets and the valuation of their liabilities.

Common valuation dates

End of December and end of March are the most common valuation dates for schemes in this tranche. Therefore, we have concentrated on these dates in this analysis.

5 and 6 April are also quite common valuation dates. We have not presented analysis at these dates. However, market conditions at 5 and 6 April 2021 were similar to those at 31 March 2021.

Bond yields

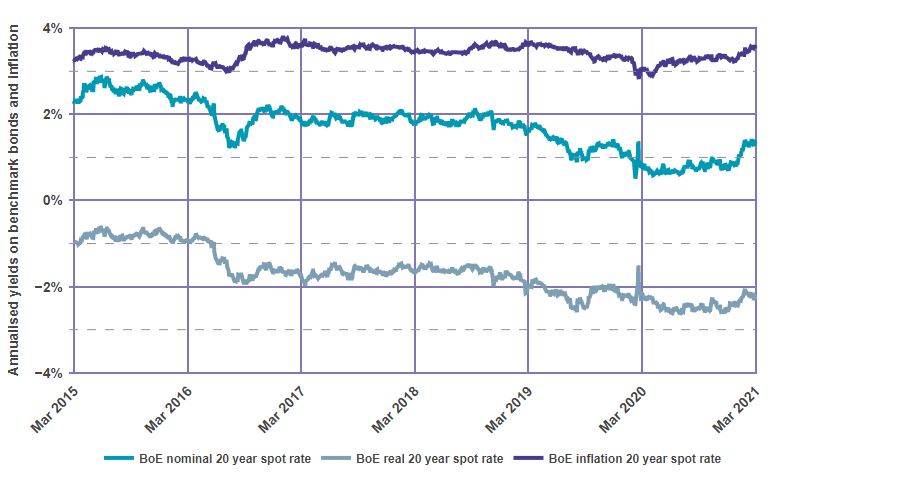

Figure 1 shows the Bank of England (BoE) estimates of nominal and real gilt yields and implied inflation as measured by the Retail Prices Index (RPI) at a 20-year duration at each date from March 2015 to 31 March 2021.

Figure 1: Benchmark yields

Sources: Bank of England (BoE), Refinitiv

There has been a fall in gilt yields since March 2015. Long-term real gilt yields fell into negative territory in 2014 and have remained negative ever since. Nominal yields have fallen in the same fashion.

Long-term market-implied inflation has remained mainly in the range 3% – 4% per annum over the six-year period.

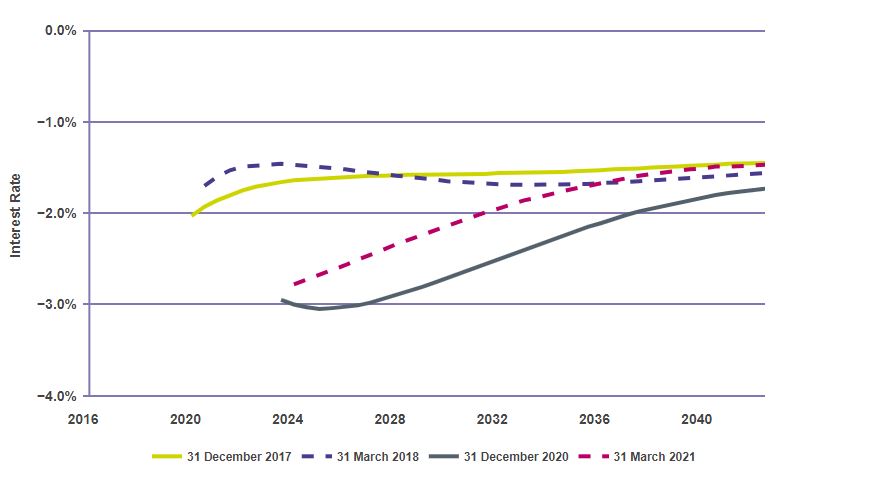

Figure 2 shows the real forward interest rates as estimated by the BoE as at the end of December 2017, March 2018, December 2020 and March 2021.

Figure 2: UK instantaneous real forward gilt curves

Sources: BoE

This chart shows that, over the periods December 2017 to December 2020 and March 2018 to March 2021, the implied real forward interest rate curve has changed shape from being relatively flat to being upward sloping. Between December 2017 and December 2020 there was a significant fall in real interest rates along the whole curve. Between March 2018 and March 2021 there was a significant fall in real interest rates in the short end of the curve, with similar yields in the middle and a small rise in real interest rates at the long end of the curve.

All other things being equal, we expect that if trustees use a discount rate to calculate liabilities that has the same margin above gilt yields at the previous valuation, most schemes will have a higher reported value for their liabilities than they were expecting.

Asset returns

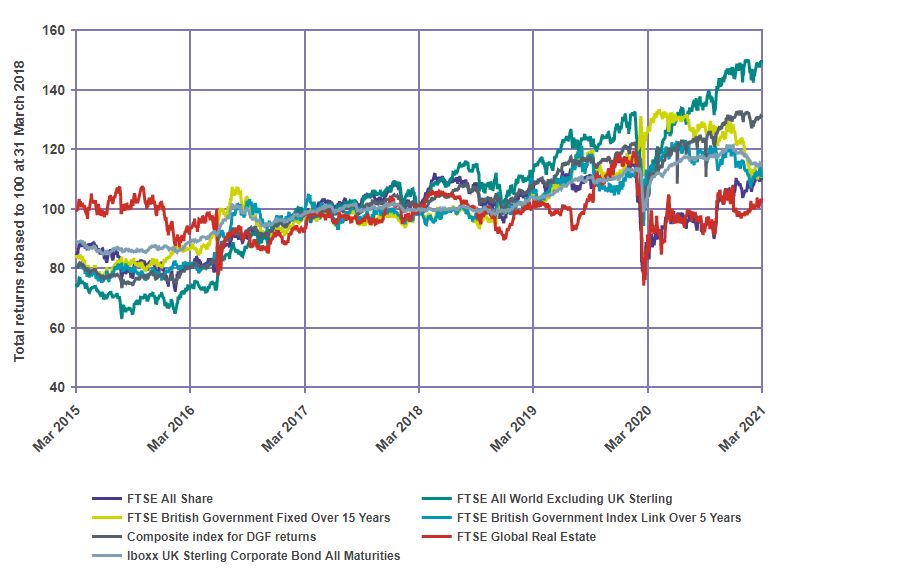

Figure 3 shows total returns for a range of asset class indices since 2015. The returns have been re-based to 100 at 31 March 2018, so the chart shows the relative change up to and from that point.

Figure 3: Asset returns

Sources: Refinitiv

Table 1: Total returns in UK Sterling from different asset classes over the three years to 31 December 2020 and 31 March 2021

^ = This index is 60% of the FTSE All World United Kingdom Sterling Index, 20% of the iBoxx United Kingdom Sterling Corporate All Maturities Total Return Index and 20% FTSE British Government Fixed All Stocks Total Return Index.

| Index name (Asset class) |

Total returns over the period 31 December 2017 to 31 December 2020 |

Total returns over the period 31 March 2018 to 31 March 2021 |

|---|---|---|

| FTSE All Share (UK equities) |

-2.7% | 9.9% |

| FTSE All World Excluding UK Sterling (Overseas equities) |

35.8% | 47.1% |

| Iboxx UK Sterling Corporate Bond All Maturities (Corporate Bonds) |

17.9% | 14.5% |

| FTSE British Government Fixed Over 15 Years (Fixed interest gilts) |

27.9% | 10.4% |

| FTSE British Government Index Link Over 5 Years (Index linked gilts) |

19.5% | 11.0% |

| Composite DGF index^ | 26.9% | 31.4% |

| FTSE Global Real Estate (Property) |

-4.5% | 2.5% |

Over the three years to December 2020, most asset classes saw positive returns, except for UK equities and property. Over the three years to March 2021 all assets classes shown above saw positive returns.

DB schemes

Funding position of DB schemes in aggregate

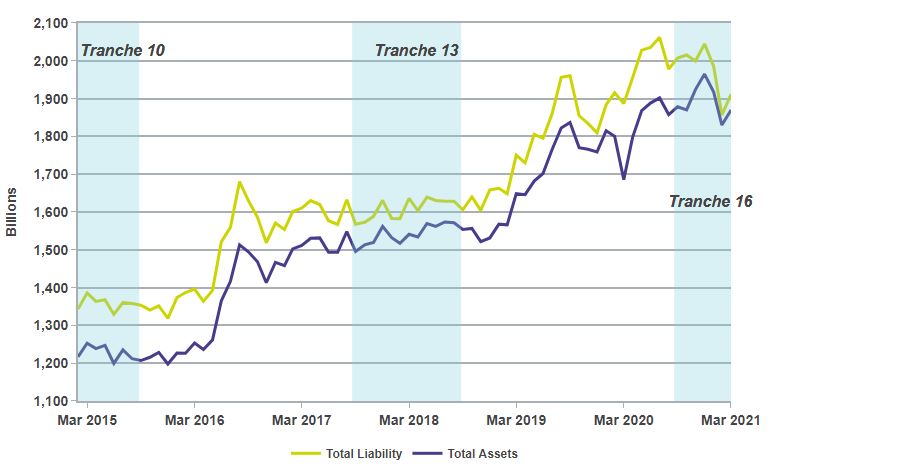

Figure 4 shows estimates of assets and liabilities (TPs) for all schemes in our regulated DB universe, based on rolling back and projecting forward the data we held at 30 September 2020 (rather than using historical data at historical dates). This is an aggregate analysis based on highly summarised data. In previous years we have shown a graph which plotted daily movements based on interpolation over a large period of time. We have updated our model and now produce a more accurate projection at monthly intervals but no longer interpolate on a daily basis between these points.

Figure 4: Estimated assets and liability positions of DB pension schemes

Sources: TPR, Refinitiv (financial markets data)

Overall, the changes in market conditions and aggregate pace of schemes’ funding plans mean that deficits on a TPs basis for the DB universe are expected to be higher at December 2020 than at December 2017. Deficits at March and April 2021 are expected to be lower than those three years earlier and some schemes will have moved into surplus.

Potential impact on scheme deficits in more detail

The analysis above showed how funding levels have changed for all schemes in the DB universe. This may not be representative of the tranche of schemes undertaking valuations now (Tranche 16). Figures 5a and 5b illustrate the key drivers in the change in deficit for all Tranche 16 schemes at the two most common valuation dates – 31 December and 31 March.

We have assumed that the discount rates that are used to calculate the liabilities of each scheme have changed since the previous scheme valuations broadly in line with three factors:

a. the movement in real and nominal gilt yields over the period

b. the movement in investment portfolios from growth-seeking to matching assets, and

c. a change in the expected return on assets above the gilt yield

For the analysis over the three years to 31 December 2020, as in previous years we have seen evidence to support a small reduction in the expected returns in excess of gilt yields as a result of schemes investing in more matching assets. We have also considered how discount rates may have changed as a result of changes in expected returns on return-seeking assets since the previous scheme valuation and have concluded there is an increase in the expected return on return-seeking assets. We have estimated that the two factors offset each other as at 31 December 2020 resulting in a zero item in Figure 5a for ‘change in relative expected outperformance’.

For the analysis over the three years to 31 March 2021, as in previous years, we have seen evidence to support a small reduction in the expected returns in excess of gilt yields as a result of schemes investing in more matching assets. We have also considered how discount rates may have changed as a result of changes in expected returns on return-seeking assets since the previous scheme valuation. We have used liability discount rates with a slightly higher margin above gilt yields than at each scheme’s previous valuation date, which partially offsets the impact of the de-risking giving an overall reduction in the margin above gilts of 0.1% per annum (compared to 0% as at 31 December 2020). This has resulted in a small item in Figure 5b called ‘change in relative expected outperformance’.

In practice, schemes may use different approaches to setting discount rates and may also have different views now on prudent expected returns from the same portfolio than they had at the previous valuation.

In addition to consideration of financial assumptions, our analysis assumes that the mortality base table assumption is updated from using the SAPS2 tables in Tranche 13 valuations to using the SAPS3_M table for Tranche 16 valuations. Also, we assume, future improvements are updated to use the latest Continuous Mortality Investigation (CMI) projections[1]. For the purpose of this analysis, we have not attempted to quantify the potential impact of COVID-19 on schemes’ mortality experience or assumptions. Given the uncertainty regarding future longevity improvements, as was explained in the AFS, we have not considered what, if any, adjustment is appropriate to apply to the CMI 2020 projections.

For the purpose of this analysis, to estimate the level of hedging we use PV01 and IE01 data, provided along with a scheme’s asset data. If these aren’t available, we make an assumption based on the scheme’s asset portfolio as to the extent of interest rate and inflation hedging.

The method used to estimate the movement in the deficits over the three-year periods presented below is necessarily simplistic. We expect scheme actuaries to have access to more detailed scheme data, which will allow a more in-depth reconciliation to take place. The method and simplifications we have made in these reconciliations are contained in the ‘methods, principal assumptions and limitations’ appendix.

In Figures 5a and 5b, the starting deficit for all schemes has been notionally set to 100 to allow for easy comparison of the change over the period. The size of the bars shown on the chart illustrates the relative impact of each of those items on the deficit over the period. As deficits decrease and schemes move into surplus we will review how we set the starting deficit.

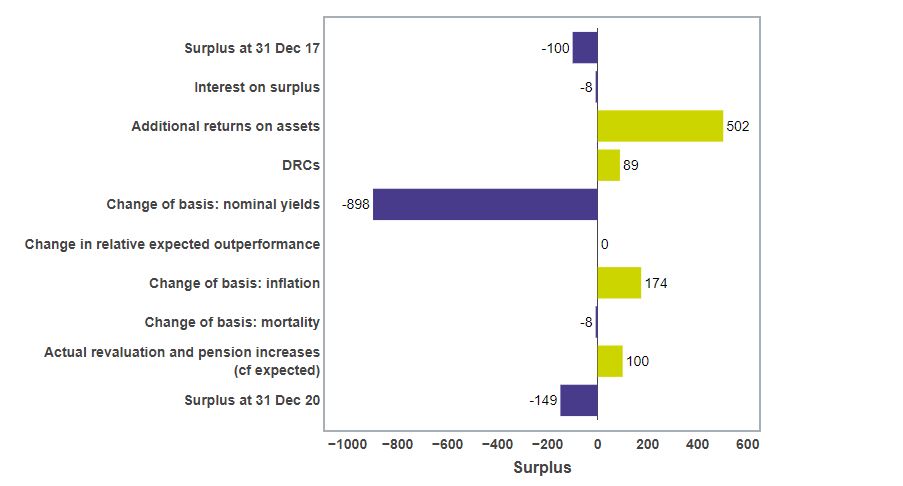

Figure 5a: Estimated impact of market conditions on deficits of all Tranche 16 schemes – December 2017 to December 2020

Sources: TPR, Refinitiv

We estimate that the aggregate deficit of Tranche 16 schemes as at 31 December 2020 would have increased from three years ago, although the funding level has remained broadly unchanged. This is because the large increase in liabilities due to changes in nominal yields and small increase due to mortality improvements were greater than the DRCs, expected asset returns and the reduction in actual and expected inflation. The impact from hedging is shown in the additional return on assets item and not the change of basis: notional yields or change of basis: inflation items. For the purpose of this analysis, we have not attempted to quantify the potential impact of COVID-19 on schemes’ mortality experience or assumptions.

However, it is expected that deficits have decreased since 31 December 2020.

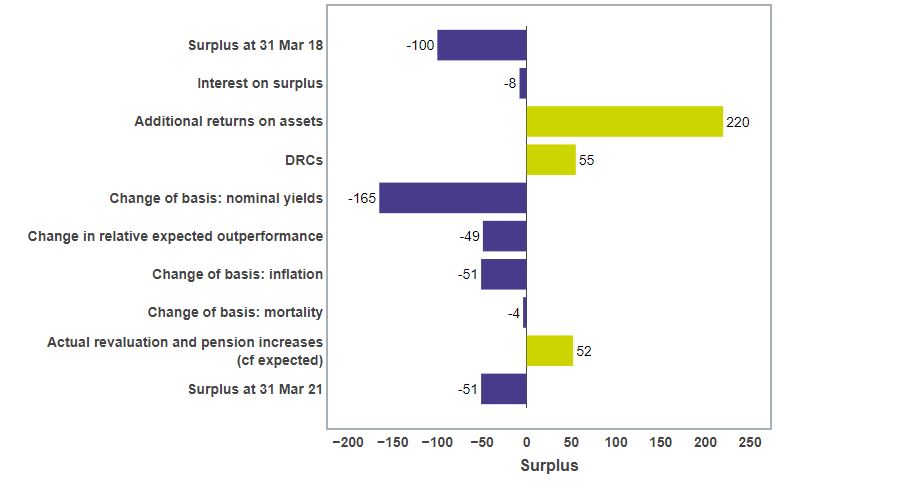

Figure 5b: Estimated impact of market conditions on deficits of all Tranche 16 schemes – March 2018 to March 2021

Sources: TPR, Refinitiv

We estimate that the funding position of Tranche 16 schemes as at 31 March 2021 would have improved from three years ago. This is mainly due to financial market movements over the three months to 31 March 2021. Real interest rates have increased across the yield curve and asset returns have been positive, with the exception of gilts and corporate bonds. For the purpose of this analysis, we have not attempted to quantify the potential impact of COVID-19 on schemes’ mortality experience or assumptions.

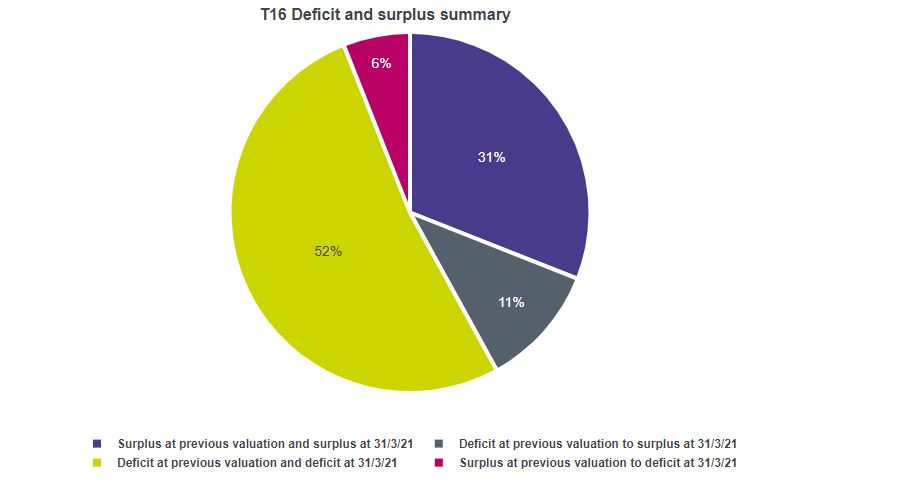

In Figure 6 below we have shown the proportion of Tranche 16 schemes which we expect to be in deficit or surplus on a TPs basis as at 31 March 2021 compared to the position at the previous valuation date.

Figure 6: Estimated number of Tranche 16 schemes in deficit/surplus at previous valuation and March 2021

Sources: TPR, Refinitiv

We estimate that 42% of schemes are in surplus on a TPs basis at 31 March 2021. The method and simplifications we have made in this analysis are contained in the ‘methods, principal assumptions and limitations’ appendix.

Variation of impact on scheme deficits – all schemes

The analysis above will not be representative of the impact of market conditions on individual schemes. Different schemes will have had different experiences depending on their individual investment strategies and funding plans.

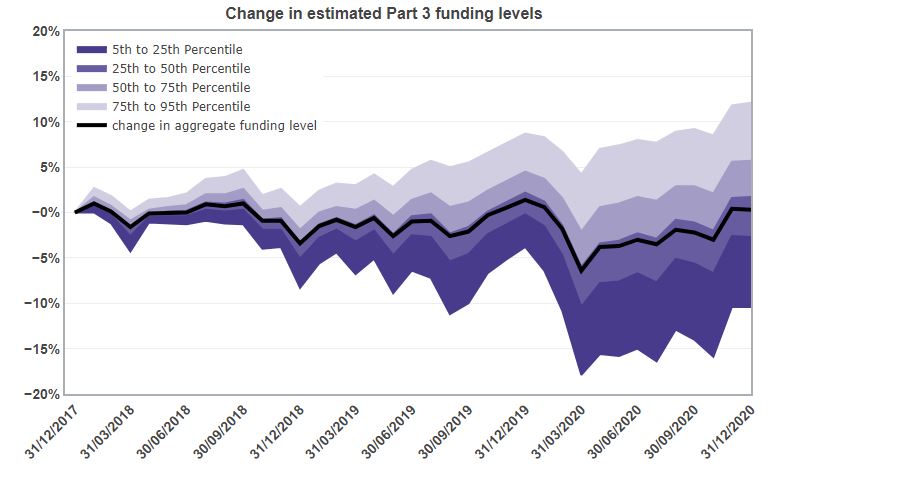

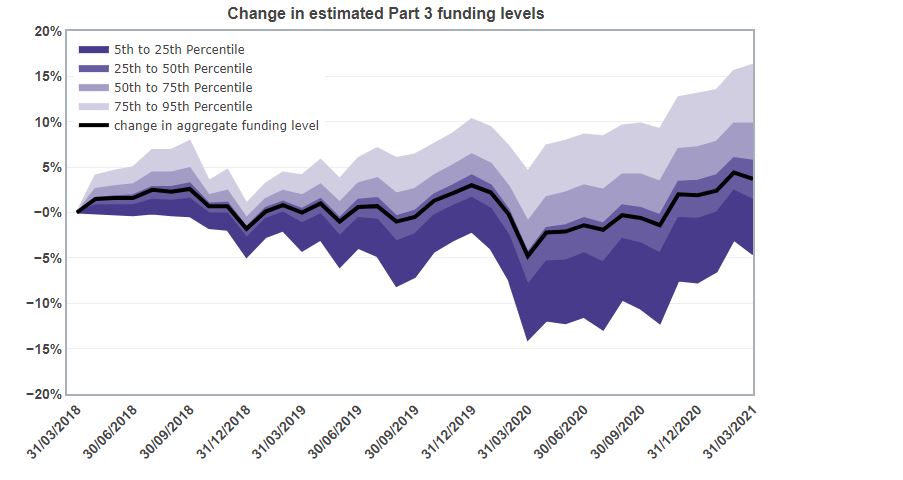

We have illustrated this variation in Figures 7a and 7b. These illustrations estimate how the funding level of each scheme has changed over the three-year period to 31 December 2020 (Figure 7a) and to 31 March 2021 (Figure 7b). Note that these illustrations show changes in funding level and not the funding levels themselves.

Figure 7a: Variation of impact of market conditions on deficits of all schemes – December 2017 to December 2020

Sources: TPR, Refinitiv (financial markets data)

The average funding level at 31 December 2020 (the black line in Figure 7a) was broadly unchanged compared to three years earlier, as has already been illustrated in the earlier analysis (for example Figures 4 and 5a). However, the experience of individual schemes varied significantly. Five percent of schemes saw estimated funding levels fall by more than 10%, whereas 5% of schemes saw estimated funding levels rise by more than 12% over the three-year period.

Figure 7b: Variation of impact of market conditions on deficits of all schemes – March 2018 to March 2021

Sources: TPR, Refinitiv (financial markets data)

Over the three-year period to 31 March 2021, the average funding level (the black line in Figure 7b) rose by around 4%, as has already been illustrated in the earlier analysis (for example Figures 4 and 5b). However, the experience of individual schemes has varied significantly, but for the vast majority of schemes was positive. Five percent of schemes saw funding levels fall by more than 5%, whereas 5% of schemes saw funding levels rise by more than 16% over the three-year period.

The most significant factors in driving the variation of experience between schemes are the extent to which schemes hedge interest and inflation rates and the extent to which schemes are invested in growth asset classes (eg equity and property). At 31 December 2020 schemes that had hedged interest rate and inflation risks appeared to have slightly improved funding levels while unhedged schemes were behind targets.

During the first quarter of 2021, equities rose both in the UK and globally while the prices of bonds and gilts fell. Consequently, the yield on gilts has risen, and to a lesser extent so have the inflation expectations of investors in the gilts market. Given the above, we expect aggregate funding positions as at 31 March 2021 to be more favourable compared with December 2020 (especially for unhedged schemes that may previously have been behind target). The worsening of the funding position between February 2021 and March 2021 includes a 0.1% reduction in the margin assumed above gilts when setting the discount rate.

Employer trends

As well as the impact of market conditions on a scheme, changes in the strength of the employer covenant are a key consideration for trustees and employers when considering funding plans and integrated risk management (IRM).

In previous years’ analysis, with the exception of last year, we have shown trends in potential employer affordability, which were based on historic publicly available information. Given the significant and uneven impact of the COVID-19 crisis on scheme employers, for many schemes recent historic trends in employer affordability are likely to be of limited use in assessing employer affordability today. Consequently, we have again excluded trends in employer affordability from this year’s analysis.

Implications for scheme funding

The analysis in this report shows that many schemes with valuations as at December 2020 are likely to have larger deficits (with funding levels broadly unchanged) than those revealed at their previous valuation date whereas those with valuation dates in March and April 2021 will have a smaller deficit than those revealed at their previous valuation date or may be in surplus.

Trustees would generally have expected their funding position to have improved over three years since their previous valuation, in accordance with their RP. However, for 31 December 2020 valuation dates, given market movements over the three-year period, it is likely that the schemes’ RPs will not be on track.

In practice, the COVID-19 crisis may have impacted the strength of the employers’ covenant, which should be reflected in the TPs. This has not been reflected in our analysis. Strengthening of TPs will increase the deficit and, if the RP end date is to be maintained, will lead to higher DRCs than our analysis shows.

The COVID-19 crisis will also have impacted the extent to which some employers can afford to make DRC payments. For some employers, affordability will have significantly reduced, at least in the short term.

Therefore, we recognise some trustees will need to make changes to their TPs and RPs to reflect changes in the strength of the employer covenant, the scheme’s funding level and changes in extent to which employers can afford to make DRC payments.

Potential impact on DRCs – scheme funding levels

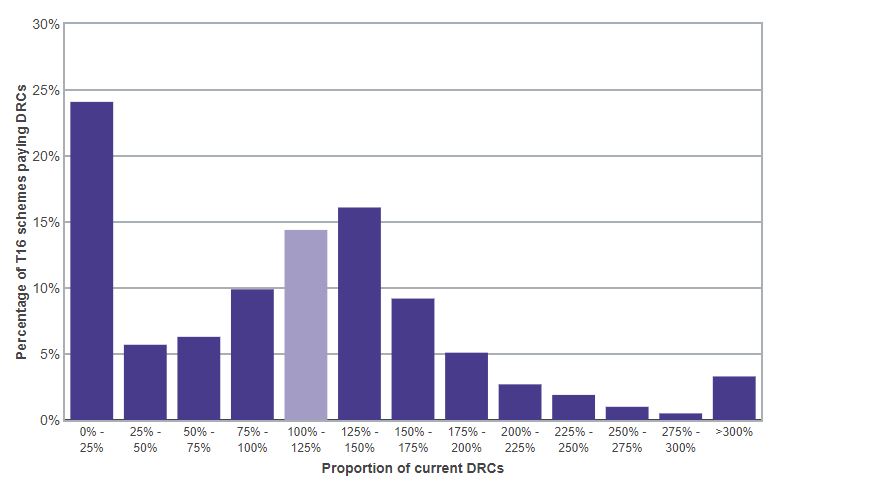

Figure 8a below illustrates the potential impact on DRCs for Tranche 16 valuations assuming a 31 March 2021 valuation date. The impact is expressed as a percentage of the level of current DRCs (ie what was agreed in Tranche 13 valuations). We have assumed, for the purpose of illustration and to remove the distorting impact of short remaining periods, that each scheme aims to eliminate the deficit over three years or the remaining term of the RP agreed at the last valuation, whichever is longer.

Figure 8a: Modelled Tranche 16 DRCs as a proportion of current DRCs – based on same RP end date as last valuation, or three years if longer

Sources: TPR, Refinitiv

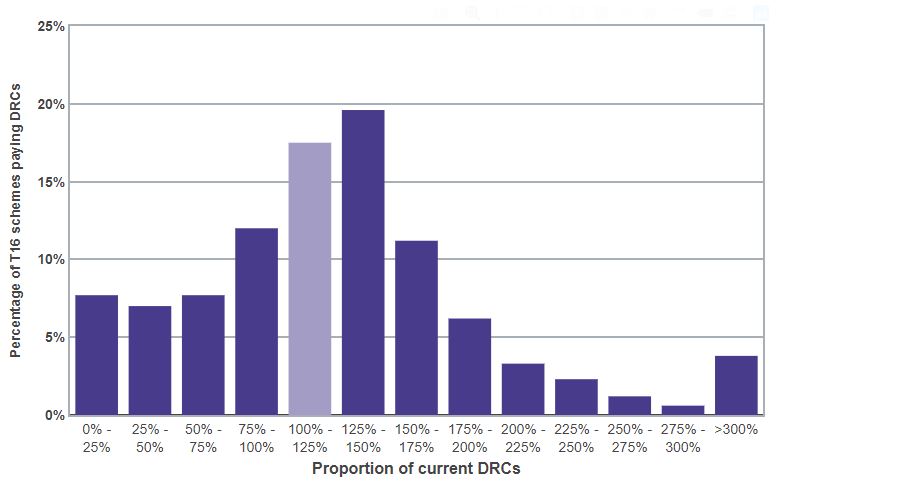

When a scheme moves from deficit into surplus, they are included in Figure 8a with a 0% proportion of current DRCs. As at lot of schemes have moved from a deficit position at the previous valuation to showing a surplus as at 31 March 2021 (see Figure 6) including them in the chart does not give a representative picture of the DRCs we expect to be paid for those schemes still in deficit. We have removed them from Figure 8b below.

Figure 8b: Modelled Tranche 16 DRCs as a proportion of current DRCs – based on same RP end date as last valuation, or three years if longer. Excludes schemes now expected to be in surplus

Sources: TPR, Refinitiv

On these assumptions around 34% of T16 schemes in deficit would be able to retain their DRCs at the same level or reduce them if their valuation date was 31 March 2021. Sixty six percent of schemes would need to increase DRCs. Around 4% would need to increase DRCs to more than three times their current levels. Some of this latter group of schemes would need to increase DRCs by a much higher factor than three.

Further examination of the schemes in the last category showed that many of them currently have shorter RPs than the average. In these cases, a relatively small increase in the RP length would lead to a much lower increase in the level of DRCs required.

This analysis does not take into account whether the TPs represent the current strength of the employer covenant, whether the current level of DRCs remain affordable nor does it consider what level of contributions is affordable.

Potential impact on DRCs - employer affordability

A key factor for trustees and employers when agreeing an appropriate RP is the affordability position of the employer, recognising that what is affordable may be affected by the employer’s plans for sustainable growth. The COVID-19 crisis may have impacted the extent to which individual employers can afford to make DRC payments. For some employers, affordability will have been significantly reduced and will be the limiting factor for DRCs, at least in the short term.

Methods, principal assumptions and limitations

Scheme data

We rely solely on the information supplied to us via scheme returns, which may not be completely up-to-date or contain the level of detail that would be available to scheme actuaries when advising trustees. This inevitably leads to many more simplifications and approximations in the methods we use to estimate aggregate and individual funding positions, compared with the more robust calculations carried out for formal valuation and RP reporting by scheme trustees.

Many of these assumptions or simplifications have been driven by data limitations. For example, we have used index tracking of major asset classes, made no allowance for detailed changes in asset strategy since the previous valuation, and made only a broad allowance for the effect of hedging instruments to mitigate interest rate or inflation risk.

Additionally, we have made assumptions about scheme liabilities in aggregate that may not accurately reflect the underlying liabilities of individual schemes.

The baseline for estimating the current deficit of each scheme is based on the results reported to us following its last valuation, adjusted approximately for contributions paid and movements in assets and liabilities in line with appropriate indices. Our analysis relies upon point-in-time valuations of schemes’ assets and liabilities. We have not allowed for any changes to the TPs to reflect any change to the employers’ covenant since the last valuation.

For the analysis over the three years to 31 December 2020, as in previous years we have seen evidence to support a small reduction in the expected returns in excess of gilt yields as a result of schemes investing in more matching assets. However, we have also considered how discount rates may have changed as a result of changes in expected returns on return-seeking assets since the previous scheme valuation and have concluded there is an increase in the expected return on return-seeking assets.

For the analysis over the three years to 31 March 2021, we have also seen evidence to support a small reduction in the expected returns in excess of gilt yields as a result of schemes investing in more matching assets. We also considered how discount rates may have changed as a result of changes in expected returns on return-seeking assets since the previous scheme valuation. We have used liability discount rates with a slightly higher margin above gilt yields than at each scheme’s previous valuation date, which partially offsets the impact of the de-risking giving an overall reduction in the margin above gilts of 0.1% per annum (compared to 0% as at 31 December 2020).

We have also made an allowance for the alignment of RPI to CPIH from 2030. Based on the average maturity of the universe of schemes and the expectation that the current RPI curve factors in the change from 2030, we have assumed that the gap between RPI and CPI will be 0.05% lower than at the previous valuation.

In addition to consideration of financial assumptions, our analysis assumes that the mortality base table assumption is updated from using the SAPS2 tables in Tranche 13 valuations to using the SAPS3_M table for Tranche 16 valuations. Also, we assume, future improvements are updated to use the latest Continuous Mortality Investigation (CMI) projections [2].

For the purposes of our aggregate analysis, to estimate the level of hedging, we use PV01 and IE01 data provided along with the scheme’s asset data. If these aren’t available, we make an assumption based on the scheme’s asset portfolio as to the extent of interest rate and inflation hedging.

When estimating the impacts on RPs, we have used the simplifying assumption that all Tranche 16 schemes have their next actuarial valuation as at 31 March 2021.

The assumptions we have made may be a significant source of difference when compared with formal valuation results at the individual scheme level. In particular, for individual schemes, the results will be highly dependent on the following:

- the exact date of valuation

- the scheme’s asset strategy, including any changes made during the inter-valuation period

- the extent of hedging against interest rates and inflation

- any changes to its mortality and longevity assumptions to reflect new information and emerging experience

- the scheme’s assessment of the appropriate discount rate and inflation assumption used to measure its liabilities

For example, if trustees choose to use discount rates that are higher than we have assumed, then the estimated liabilities and deficits are likely to be lower than those modelled in this analysis, and vice versa.

Employer and contribution data

We rely solely on the information supplied to us via scheme returns to identify our employer population, which may not be up-to-date or contain the level of detail that would be available to covenant advisers when advising their clients. This inevitably leads to many more simplifications and approximations in the methods we use to estimate aggregate and individual covenant support.

The information on DRCs we collect covers DRCs expected in each year of the associated RP, with additional information as to the date the RP began and ends. DRCs are assumed to be paid continuously: 1/365th of DRCs in year one of the RP are assumed to be paid on every day of the year.

Employer covenant

The strength of the employer covenant is an important element in scheme funding and a key part of integrated risk management. We use a number of metrics relating to employers to determine covenant risk. However, we recognise that this is a highly complex area and that a one-size-fits-all approach to looking at employer covenant would miss the many complexities and nuances of individual employers. For these reasons, we combine the use of metrics with professional judgement when assessing covenant.

Assessing the covenant is about understanding the extent to which the employer can support the scheme, now and in the future, including the risks to this support being available when it is needed. The focus should be on the ability of the employer to make cash contributions to the scheme to achieve and maintain full funding over an appropriate period, including addressing downside risks.

COVID-19 has resulted in considerable uncertainty over some employers’ covenant strength and their affordability to address deficits in schemes. However, the impact will be varied across the landscape and some businesses will recover more quickly than others.

Glossary

Deficit repair contributions (DRCs)

These are contributions made by employers to the scheme in order to address any deficit in the value of the assets compared to the technical provisions (TPs), typically in line with the Schedule of Contributions and the recovery plan (RP). For the purpose of this analysis, we have assumed current contributions to be those in year 4 of the RP agreed at the Tranche 13 valuation, except for RPs which were shorter than four years where we have assumed that the contributions paid in the last full year of the plan have continued. Throughout this analysis we have used deficit repair contributions (DRCs) in the context of the value the scheme receives without making any allowance for any tax benefit the sponsoring employer may receive.

IRM

Integrated risk management (IRM) is a risk management approach that can help to identify, manage and monitor the factors that affect the prospects of meeting scheme’s funding objectives. It involves examining how employer covenant, investment and funding risks relate to and are affected by each other. It also considers what to do if risks materialise.

Recovery plan (RP)

Under Part 3 of the Pensions Act 2004, where there is a funding shortfall at the effective date of the actuarial valuation, the trustees must prepare a plan to achieve full funding in relation to the TPs. The plan to address this shortfall is known as a recovery plan.

RP length

The RP length is the time that it is assumed it will take for a scheme to eliminate any shortfall at the effective date of the actuarial valuation, so that by the end of the RP it will be fully funded in relation to the TPs.

Technical provisions (TPs)

The funding measure used for the purposes of Part 3 valuations. The TPs are a calculation undertaken by the actuary of the assets needed at any particular time to make provision for benefits already accrued under the scheme, using assumptions prudently chosen by the trustees, and are required for the scheme to meet the statutory funding objective. These include pensions in payment (including those payable to survivors of former members) and benefits accrued by other members and beneficiaries, which will become payable in the future.

Tranches

‘Tranche’ refers to the set of schemes that are required to carry out a funding valuation within a particular time period. Schemes whose valuation dates fall between 22 September 2020 and 21 September 2021 (both dates inclusive) are in Tranche 16. Because scheme-specific funding valuations are generally required every three years, these schemes (with a few exceptions) had their last formal valuation in Tranche 13 (valuation dates between 22 September 2017 and 21 September 2018).

Footnotes

- [1] While this is appropriate for the purposes of our aggregate analysis of schemes in general, what will be appropriate for individual schemes will depend on their specific circumstances. Note, at the time the analysis was performed we used CMI 2019 projections with a long-term improvement rate of 1.5% and an A Factor of 0.5.

- [2] See previous footnote.