People’s lives are different - we must understand savers to design defaults for retirement

Default pension plans will be powerful in helping to turn a savings system into a pension system. But who are defaults designed for? Director of Strategy and Communications Patrick Coyne sets out how career breaks can impact outcomes and asks if cohorts could help those savers achieve a sustainable income in retirement.

The Pension Schemes Bill set us on a path towards default pension plans which will support people throughout retirement. They will be powerful in helping turn a savings system into a pension system.

Whilst savers’ personal circumstances vary, the best schemes, governed by skilled trustees, will think about how to use defaults to deliver better outcomes for cohorts of savers who face similar challenges.

Our new analysis shows career breaks can have a big impact on retirement outcomes. And as schemes start to think about implementing default pension plans, there’s a real opportunity for schemes to reflect predictable contribution patterns in default designs.

Building on participation to deliver outcomes

We’re building from a strong base. Auto-enrolment changed pensions.

Participation rose. 11 million more savers, people from every walk of life contributing.

Defaults worked. The vast majority, some 94%, of savers are within an investment strategy designed by trustees with the help of their professional advisers.

Scale improved governance. Master trusts, following an authorisation process, led the way.

That was the first chapter in this century’s pension reforms.

The next chapter is about outcomes. To make sure that millions of savers have a sustainable income through what we all hope are decades in retirement.

Government, in its reform agenda, has been clear: pensions should normally provide an income in retirement. And through the guided retirement duty in the Pension Schemes Bill, many are thinking about how best to deliver this ambition.

We will support the secondary legislation as it develops with new guidance to help trustees comply with their obligations.

And there is a lot of scope for innovation because the primary legislation has not been prescriptive on the model used, or when and how an income in retirement is best delivered.

How much income savers have is dependent on contributions, the investment returns and value we provide as industry, and from time and the eighth wonder of the world, compounding.

It grows, or it does not, depending on design.

Defaults are right for retirement given the complexity involved and are extremely powerful because most members do not choose. They follow the careful path we set.

But who are we designing for?

Career breaks have a significant impact on outcomes

Default design has rested on an image of the typical member: continuous employment, steady, and hopefully, increasing, earnings, a clear retirement date – often triggered by the anchor of the State Pension age.

For some people, that still holds.

For many people, it does not.

Working lives today are uneven. Contributions pause. Hours reduce. Earnings rise and fall. Caring responsibilities interrupt careers. Retirement itself is less defined.

These patterns are widespread and predictable.

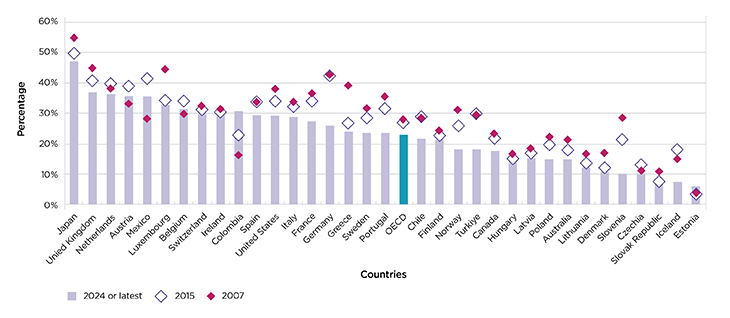

OECD evidence shows that across developed economies, women receive significantly lower pension incomes than men. Across the board, it is around 25% less.

There are a number of reasons for this. Historically, women have made fewer contributions (due to both lower pay and higher caring commitments). They have retired earlier. And they have lived longer. A triple whammy.

Interrupted contributions create predictable, long-lasting inequities

In workplace pensions, a major driver is interrupted contribution histories, most commonly driven by caring responsibilities. Lost years mean lost growth. And this is increasingly important as we head towards the 2030s where more and more people will be reliant on defined contribution pots.

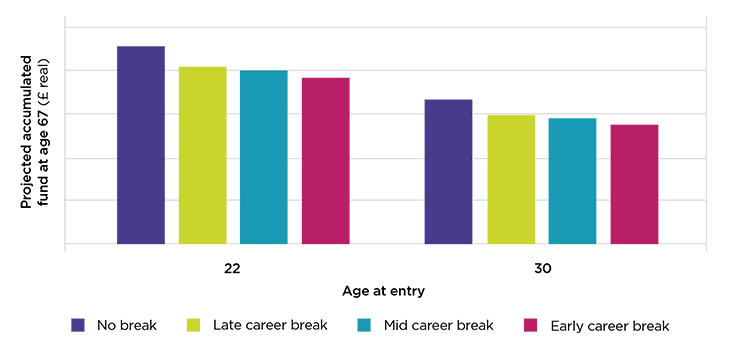

This chart, a simplified example for a median earner contributing automatic enrolment minimums, shows a pot value at age 67 under different career break scenarios.

It illustrates the impact of a five year career break, but also crucially the timing sensitivity of breaks.

It shows savers who take a career break within the first 10 years of working life face the prospect of a pot size around 16% lower. And that’s before considering the impact of a return on a part-time basis or potential impact on career progression, and wage rises, a break may have.

Earlier breaks remove contributions at the point where they would otherwise likely have the longest exposure to risk and hence returns. And because these breaks are disproportionately taken by women, and typically earlier rather than later in a career, the pattern we see is inherently an equity issue. A fairness issue.

The typical response to this is 'better communications' and an overemphasis on paying more and planning more. But as an industry could we do more to help later life outcomes?

Modest default differentiation could make a difference

Many in industry are now thinking about how to guide people towards the right retirement for them.

And if the objective from pension saving is generating a sustainable income for savers, then strategy design must reflect systemic risk.

Clearly, this does not mean individual tailoring at scale. But it does mean understanding your members and seeing if there are perhaps one or two defined cohorts, where modest differentiation could really make a difference.

Trustees and providers already hold the data, in part or in full. Contribution histories. Pot sizes. Age profiles.

And you do not need full visibility of a saver’s wider wealth to recognise the risk caused by uneven contributions. The information is there. The question is whether we use it.

We already do cohorting within our defaults. We just call it lifestyling, where we accept that a 30-year-old and a 60-year-old should probably not be on the same investment path.

I would argue that contribution patterns are just as economically significant as age. And it may be that trustees consider that those with an early career break need a different glidepath, different guardrails, and potentially different income smoothing mechanisms from a member who hasn’t.

Using the scale and might provided by a default arrangement’s investment building blocks, but tailoring it to meet the needs of people who need a different path where risk is systematically different. Small evidenced-based differentiation, building on the existing logic of glidepaths, could make a real difference, and truly demonstrates fulfilment of fiduciary obligations.

We should respond to predictable patterns of risk within our memberships

Retirement income is shaped by more than pension balances. Home ownership and household structure affects both resilience and what is 'enough', as the Pensions UK retirement living standards show.

Pension schemes can’t control these realities. But they should recognise them and communications and default retirement options should reflect the ground members are standing on, not an idealised version of it.

The guided retirement duty will bring in a new chapter for our pensions system, one focused on delivering the outcome savers need: a sustainable income in later life.

How schemes approach it will be iterative based on the different needs of the generations of people approaching retirement, and the more they learn about their members.

The UK pensions system has achieved something significant. Participation is high, governance is improving, and scale is building.

But participation is not the destination. A sustainable income in retirement is.

Default options must evolve for the reality of modern working lives. When it comes to defaults, we need to design for the members we have, not the members we once assumed.

Career breaks are common, predictable, and economically significant. Schemes that recognise this will be better placed to deliver sustainable incomes for all savers.

Patrick Coyne

Director of Strategy and Communications