Employer duties and defining the workforce: An introduction to the employer duties

Automatic enrolment detailed guidance for employers no. 1

Accompanying resources

Information to workers

Summary of information requirements in a quick-reference table format

The different types of worker

Diagram of the different categories of worker and the criteria for each category

Resource of duties and safeguards for employers

At-a-glance summary of the duties and safeguards

How to save this page as a PDF

About this guidance

This guidance is aimed at professional advisers and employers with in-house pensions professionals.

It is the first in a series of guidance that explains the employer duties and safeguards in detail. Illustrative examples throughout the series show further how the laws apply in practice.

It covers the points an employer must understand to comply with their duties from their duties start date (the date the laws apply to that employer for the first time).

This guidance tells an employer:

- how the working population is classified under the new legislation

- what is meant by ‘worker’, the different categories of worker and how to identify them

- how to assess their workforce and to identify which individuals they will have new employer duties for

- what the new duties are in relation to each category of worker

We recognise that many employers will already have pension provision for their workers, and that this will often match or exceed the minimum requirements contained in the duties. In these cases, such employers may just need to check that the minimum requirements are covered in their existing processes.

It will help employers if they are familiar with the different categories of workers. These are explained further in this guidance and a quick reminder is available in the Key terms.

This guidance forms part of the latest version of the detailed guidance for employers (published June 2021).

Changes from last version

This guidance has been updated to remove:

- out of date content relating to an employer’s staging date

- the effect on the qualifying person exception as a result of the changes to the cross-border pension requirements following the UK’s exit from the EU

Paragraph numbers have changed as a result of these amendments.

An employer must understand their duties

Introduction

- A number of new employer duties have been introduced that will give millions of workers access to pension provision, many for the first time.

- What an employer needs to do will depend on whether they employ someone the legislation classifies as a ‘worker’.

- The term ‘worker’ is specific – it does not simply apply to the working population as a whole. There are different categories of worker, determined by a person’s age and how much they earn.

- A key requirement is to automatically enrol certain workers, known as eligible jobholders, into a pension scheme that meets specific conditions to be an ‘automatic enrolment scheme’. More information on the conditions to be an automatic enrolment scheme can be found in Detailed guidance no. 4 – Pension schemes. However, automatic enrolment is only one of the duties.

- For all employers, compliance with the new employer duties and safeguards is compulsory. It is crucial that all employers understand how their workforce is categorised under the new legislation.

- An employer needs to know:

- the criteria that determine whether someone is considered as a ‘worker’

- the criteria that determine what category of ‘worker’ that person is

- They also need to be able to apply this in practice to their own workforce so they can be compliant with the new duties.

Identifying whether a person is a ‘worker’

- The first step for an employer is to see if they employ anyone classed as a ‘worker’. To do this, they need to understand their contractual relationships.

- A worker is defined as any individual who:

- works under a contract of employment (an employee), or

- has a contract to perform work or services personally and is not undertaking the work as part of their own business.

- Anyone who has entered into a contract of this type with an individual is an employer and is required to comply with the new employer duties.

- This may include agency workers if they have such a contract with either the agent or the principal (the third party to whom the individual is being supplied by the agent). Broadly, agency workers are individuals who are supplied by an agent to work for a third party (the principal) under a contract or arrangement between the agent and the principal, and who are not undertaking the work as part of their own business. For example, a person taken on by a recruitment agency that gives that person a temporary assignment to work for someone else.

- In the absence of a worker’s contract between the agency worker and the agent or principal, the agency worker may still be a worker for the purposes of the new duties (see paragraphs 20-21).

- The final point to note about the definition of worker in paragraph 9 is that the physical location of the employer is not a determining factor when considering an individual’s status as a worker, eg the employer may be based outside the UK.

- The following sections set out more detail. There are a small number of exemptions from the definition of a worker, set out in paragraphs 29-39.

A note about contracts

- a contract does not have to be in writing

- it can be a verbal contract between the employer and the worker

- the terms of employment can be implied, rather than explicitly stated

- multiple contracts with one individual will require additional assessment to establish if they are separate contracts or if they should be treated as a single employment relationship Detailed guidance no. 3 – Assessing the workforce has more information

- where a transfer occurs under the Transfer of understandings protection of employment (TUPE) regulations, transferred-in workers should be viewed as being under a new contract and the new employer should therefore assess that individual’s worker status at the point of transfer

Personal service workers

- If an individual does not work under a contract of employment, they may still be assessed as a worker for the purposes of the new duties if they have contracted to perform work or services personally, other than as part of their own separate business (’ a personal services worker’). However, an individual who is paid a fee as a self-employed contractor under a contract for services is not normally a worker.

- The distinction between such a self-employed contractor and a personal services worker is much debated in employment law and employers will be used to making the assessment of employee status for employment rights and tax purposes.

- However, employers should not rely solely on a person’s tax status when assessing whether they are a worker. An individual considered by HM Revenue & Customs (HMRC) as self-employed for tax purposes may still be classed as a ‘worker’ under the new employer duties legislation, if they are in fact working under a contract to perform work or services personally, other than as part of a separate business of their own.

- No single factor, by itself, is capable of being conclusive in determining whether an individual is a personal services worker. However, individuals are likely to be considered as such if most, or all, of the following statements are true:

- the employer relies on the individual’s expertise and expects them to perform the work themselves

- there is an element of subordination between the employer and individual, for example the individual reports to the employer’s managers or directors in respect of the specific operation or project on which they are contracted to work

- the contractual provisions state that the contract is not a contract for services between the employer and the individual’s own business

- the contract provides for employee benefits such as holiday pay, sick pay, notice, fees, expenses etc

- there is a mutual obligation set down in the contract to provide or do the work

- the individual does not incur any financial risk in carrying out the work

- the employer provides tools, equipment and other requirements to the individual to carry out the work

- This list is not exhaustive. As when they are assessing an individual’s status for tax purposes, an employer must take into account all relevant considerations.

Agency workers

- Where there is no worker’s contract between the agency worker and the agent or the principal, an agency worker (as defined in paragraph 11) is treated as a worker for the purposes of the new duties.

- The agent or principal will be the agency worker’s employer depending on which is responsible for paying the worker under any arrangement between the agent and the principal. Consequently, whichever is responsible will be subject to the employer duties. If it cannot be determined who is responsible for paying the worker, for example, if the contract or arrangement between the principal and agent did not cover this particular issue, then whichever actually pays the worker will be the employer.

Secondees

- Individuals working on secondment from another company will usually remain a worker for the company from which they are seconded.

- Therefore, an employer with a secondee is unlikely to have any employer duties in relation to that individual, but the employer who has seconded their worker usually will.

- However, employers should examine the contractual and remuneration arrangements for secondees to ensure the correct party carries out the employer duties.

Seafarers

- Any person employed or engaged in any capacity on board a ship or hovercraft is to be treated as if they were a worker.

Offshore workers

- Offshore workers are people who are working in the territorial waters of the UK or in connection with the exploration of the sea bed or subsoil, or the exploitation of their natural resources, in the UK sector of the continental shelf (including the UK sector of a cross-boundary petroleum field).

- They will need to be assessed in the same way as other individuals and will be classed as a worker if they meet the criteria in paragraph 9.

Persons who are not workers

- As described in paragraph 15, an individual working under a contract for services with the employer (ie as a self-employed contractor) is not normally a worker. In addition, there are a few situations where one or more individuals are employed, but they are not classified as workers. Employer duties do not apply to these people.

Directors

- If an individual is a director of a company and the company has no other employees, that individual is not a worker by virtue of any office that they hold or contract of employment under which they work. The company is therefore not subject to the employer duties in relation to that individual.

- Similarly, if the company has more than one director, none of whom have a contract of employment with the company, none of the directors is a worker and the company is not subject to employer duties in relation to those directors. But if two or more directors have a contract of employment with the company, those directors will become workers. The company will have automatic enrolment duties in relation to them, with the modifications explained in paragraphs 107 to 109 below.

- Where the company takes on one or more workers in addition to the directors, the company will have employer duties in relation to those workers, but will not have duties in relation to any of the directors unless the directors have contracts of employment with the company. Again where the company has duties in relation to any director, these will be modified as set out in paragraphs 107 to 109 below.

- These rules apply to anyone holding office as a director. This does not include a person who is a director in name only. In the case of a company, it means a director formally appointed under the Companies Act 2006, and also anyone acting as a director in the sense of having a decision-making role in the corporate governance of the company even if they have not been properly appointed. In the case of corporate bodies other than companies, it means anyone holding an office of director created by the establishing legislation or Royal Charter.

Armed forces

- Any serving member of the naval, military or air forces of the Crown is not classified as a worker.

- Members of the following forces are not workers when they are carrying out their duties as members of that force:

- Combined Cadet Force

- Sea Cadet Corps

- Army Cadet Force

- Air Training Corps

Employers need to understand contractual relationships

Office-holders

- An office-holder is not normally a worker.

- An office-holder has no contract or service agreement in relation to their appointment, nor do they usually receive a salary or regular remuneration for their services. They may however, be paid a fee for their services or to cover their expenses.

- Examples of office-holders who are not normally workers include:

- on-executive directors

- company secretaries

- board members of statutory bodies

- trustees

- It is very important to consider the specific circumstances of the individual. Sometimes a person who appears to be an office-holder may also have a contract of service for part of their duties and will therefore be a worker in respect of those duties. The particular position of directors is discussed in paragraphs 29 to 32 above and 104 to 106 below.

Volunteers

- Volunteers would not normally have a contract of service and are not workers. However, this may change if any form of payment or non-financial benefit is given to them.

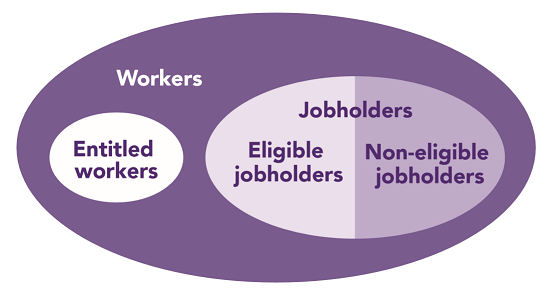

The different categories of ‘worker’

- Once an employer has identified that they have a worker, the next step is to ascertain what type of worker they have. It is only in respect of certain types of workers that an employer will have duties.

- There are two main categories of worker for which the employer duties apply:

- jobholders

- entitled workers

- The category of jobholder then further subdivides into two groups:

- eligible jobholders

- non-eligible jobholders

- Figure 1 illustrates how the different categories of worker relate to each other. (Note that the size of the components is not indicative.)

Figure 1: The different categories of worker

- The employer duties apply in respect of:

- eligible jobholders

- non-eligible jobholders

- entitled workers

- The duties are different for each of these categories and are described in the section called Employer duties and safeguards.

- The category into which a worker falls is determined by their age and whether they earn qualifying earnings.

Eligible jobholders

- They are called this because they are ‘eligible’ for automatic enrolment. These are workers who:

- are aged at least 22 but under state pension age

- are working or ordinarily work in the UK under their contract

- have qualifying earnings payable by the employer in the relevant pay reference period that are above the earnings trigger for automatic enrolment

Non-eligible jobholders

- They are called this because they are not eligible for automatic enrolment but can choose to opt in to a pension scheme. These include workers who either:

- are aged between 16 and 74

- are working or ordinarily work in the UK under their contract

- have qualifying earnings payable by the employer in the relevant pay reference period but below the earnings trigger for automatic enrolment

or

-

- are aged between 16 and 21, or state pension age and 74

- are working or ordinarily work in the UK under their contract

- have qualifying earnings payable by the employer in the relevant pay reference period that are above the earnings trigger for automatic enrolment

Jobholders

- Together, non-eligible jobholders and eligible jobholders make up the jobholders group. So, jobholders are workers who:

- are aged between 16 and 74

- are working or ordinarily work in the UK under their contract

- have qualifying earnings payable by the employer in the relevant pay reference period

Entitled workers

- They are called this because they are ‘entitled’ to join a pension scheme. These are workers who:

- are aged between 16 and 74

- are working or ordinarily work in the UK under their contract

- do not have qualifying earnings payable by the employer in the relevant pay reference period

Summary of worker category

- Table 1 illustrates the categories relative to age and earnings for workers who are working or ordinarily work in the UK.

- Detailed guidance no. 3 – Assessing the workforce explains the steps an employer must take to correctly identify the category of worker, in particular how to assess whether a worker is working or ordinarily works in the UK and whether qualifying earnings are payable to a worker in the relevant pay reference period.

Table 1 - Categories of worker relative to age and earnings

| Earnings | Age (inclusive) | ||

|---|---|---|---|

| 16-21 | 22-State pension age (SPA) | SPA-74 | |

| Lower earnings threshold or below | Entitled worker | ||

| More than lower earnings threshold up to and including the earnings trigger for automatic enrolment | Non-eligible jobholder | ||

| Over earnings trigger for automatic enrolment | Non-eligible jobholder | Eligible jobholder | Non-eligible jobholder |

Employer duties and safeguards

- All employers with at least one worker, regardless of their age or earnings, must:

- declare their compliance with The Pensions Regulator. This is an online process. You can find out more about it in our simple steps for employers

- adhere to the safeguards. More information on the safeguards can be found in paragraphs 79-82

- If the employer has workers and chooses to use postponement, they will also need to give their workers information about how postponement affects them. (An employer can use postponement to postpone the relevant employer duty for the worker for a period of up to three months. Postponement is described in Detailed guidance no. 3a – Postponement.)

- The employer duties for each category of worker are described next and table 2 provides a summary.

Eligible jobholders

- An employer must automatically enrol an eligible jobholder into an automatic enrolment scheme on the eligible jobholder’s automatic enrolment date (or deferral date, where postponement has been used). Identifying the automatic enrolment date is explained in Detailed guidance no. 3b – Having completed the assessment. The deferral date is explained in Detailed guidance no. 3a – Postponement.

- Part of the automatic enrolment process also requires an employer to give the eligible jobholder information telling them:

- they have been, or will be, automatically enrolled and what this means for them

- their right to opt out and their right to opt back in

- The employer will also have to give information about the eligible jobholder to the scheme.

- Full details of this information can be found in Detailed guidance no. 5 – Automatic enrolment.

- The eligible jobholder may choose to opt out of scheme membership once they have been automatically enrolled. ‘Opting out’ has a specific meaning in the new employer duties. It refers to the provision of a mechanism under the law which has the effect of undoing active membership, as if the worker had never been a member of a scheme on that occasion. It can only happen within a specific time period know as the ‘opt-out period’. More information on opt-outs can be found in Detailed guidance no. 7 – Opting out.

- An employer will continue to have responsibilities towards the individual who has opted out. One of these is to automatically re-enrol them every three years, if they are still an eligible jobholder working for that employer.

- The employer must pay employer contributions to the scheme.

Non-eligible jobholders

- Non-eligible jobholders do not meet the additional criteria to be eligible jobholders, so do not need to be automatically enrolled. However, they have a right to opt in to an automatic enrolment scheme, if they choose, so an employer still has duties in relation to them.

- An employer must give their non-eligible jobholders certain information about both the right of a jobholder to opt in to an automatic enrolment scheme and the right of an entitled worker to join a pension scheme.

- The employer must give this information to the non-eligible jobholder within six weeks of the earlier of the date on which they become a non-eligible jobholder or the date they become an entitled worker, eg the employer’s duties start date or, if after their duties have started to apply, the non-eligible jobholder’s first day of employment.

- This requirement does not apply if the employer has previously given this information, for example because the employer chose to use postponement in respect of the non-eligible jobholder and gave them a postponement notice.

- If a non-eligible jobholder chooses to opt in to a pension scheme, they must do so by giving the employer an ‘opt-in notice’. On receipt of a valid opt-in notice, the employer must enrol the noneligible jobholder into an automatic enrolment scheme by following the automatic enrolment process.

- The employer must pay employer contributions to the scheme.

- Detailed guidance no. 6 – Opting in, joining and contractual enrolment provides more detail.

Entitled workers

- Entitled workers do not need to be automatically enrolled. However, they do have a right to join a pension scheme. The pension scheme the employer chooses to use can be a different scheme to the one they may be using for automatic enrolment.

- An employer must give their entitled workers certain information about both the right of a jobholder to opt in to an automatic enrolment scheme and the right of an entitled worker to join a pension scheme.

- The employer must give this information to the entitled worker within six weeks of the earlier of the date on which they become a non-eligible jobholder or the date they become an entitled worker, eg the employer’s duties start date or, if after their duties have started to apply, the entitled worker’s first day of employment.

- This requirement does not apply if the employer has previously given this information for example because the employer chose to use postponement in respect of the entitled worker and gave them a postponement notice.

- If an entitled worker chooses to join a pension scheme, they must do so by giving the employer a ‘joining notice’. The employer must then arrange membership of a scheme for them.

- The employer will have to deduct contributions on behalf of the entitled worker and pay these into the scheme.

- However, the employer does not have to pay into the scheme themselves, unless they choose to do so, or have chosen a scheme that requires an employer contribution.

- Detailed guidance no. 6 – Opting in, joining and contractual enrolment provides more detail.

How the categories relate and what the employer must do for each

- Table 2 sets out the different categories of worker and illustrates what the employer must do (including the employer duties) for each.

Table 2: Categories of workers and what the employer must do for each

| Category of worker | What the employer has to do | Related guidance |

|---|---|---|

| Eligible jobholder |

|

Detailed guidance no. 5 – Automatic enrolment |

| Process any opt-out notice | Detailed guidance no. 7 – Opting out | |

| Automatically re-enrol approximately every three years or immediately if specific events caused active membership to cease | Detailed guidance no.11 – Automatic re-enrolment | |

| Keep records of the automatic enrolment process | Detailed guidance no. 9 – Keeping records | |

| If using postponement, give a notification to the eligible jobholder | Detailed guidance no. 3a – Postponement | |

| Non-eligible jobholder | Give information about the right of a jobholder to opt in and the right of an entitled worker to join | Detailed guidance no. 10 – Information to workers |

|

If the non-eligible jobholder decides to opt in:

|

Detailed guidance no. 6 – Opting in, joining and contractual enrolment | |

| Process any opt-out notice | Detailed guidance no. 7 – Opting out | |

| Keep records of the enrolment process | Detailed guidance no. 9 – Keeping records | |

| Automatically re-enrol if specific events caused active membership to cease | Detailed guidance no.11 – Automatic re-enrolment | |

| Entitled worker | Give information about the right of a jobholder to opt in and the right of an entitled worker to join | Detailed guidance no. 10 – Information to workers |

| If the entitled worker decides to join, arrange pension scheme membership | Detailed guidance no. 6 – Opting in, joining and contractual enrolment | |

| Keep records of the joining process | Detailed guidance no. 9 – Keeping records | |

| Worker | If using postponement at their duties start date or the worker’s first day of employment, give a notification to the worker. | Detailed guidance no. 3a – Postponement |

Important reminder

If the employer has one or more workers, they must complete a declaration of compliance with the regulator no later than five months after their duties start date. More details about this process and a full list of the employer duties are available on our website.

Safeguards for all workers

- There are a number of safeguards in place to protect the rights of individuals to have access to pension saving. These apply to all workers, irrespective of their category, although as with the duties, different safeguards apply to different categories of workers.

- The safeguards are listed below and Detailed guidance no. 8 – Safeguarding individuals provides further information.

- The safeguards mean employers must ensure the following:

- they do not take any action or make any omission by which the eligible jobholder ceases to be an active member of the qualifying scheme. For more information about the criteria that must be met for a scheme to be a qualifying scheme, see Detailed guidance no. 4 – Pension schemes

- they do not take any action or make any omission by which the scheme ceases to be a qualifying scheme

- they do not take any action for the sole or main purpose of inducing a jobholder to opt out of a qualifying scheme, or a worker to give up membership of a pension scheme (this is known as ‘inducement’)

- during recruitment, they or their representatives do not ask any questions or make any statements that either states or implies that an applicant’s success will depend on whether they intend to opt out of the pension scheme (this is known as ‘prohibited recruitment conduct’)

- they do not breach employment rights for individuals not to be unfairly dismissed or suffer detriment on grounds related to the new employer duties

How the categories relate and what is prohibited for an employer for each

- Table 3 sets out the different categories of workers and illustrates what the employer must not do (including the safeguards) for each.

Table 3: Categories of worker and what the employer must not do

| Category of worker | Safeguards applicable |

|---|---|

| Eligible jobholder | All |

| Non-eligible jobholder | All |

| Entitled worker |

|

| Any other worker |

|

Exceptions from the employer duties in specific circumstances

- In certain circumstances the employer duties in relation to an eligible jobholder, non-eligible jobholder or entitled worker are changed or do not apply. This is the case where the conditions for any of the exceptions from the duties are met. The safeguards continue to apply in relation to the worker as usual.

- The exceptions are:

- a worker who has opted out or ceased active membership of a qualifying scheme

- a worker who has given notice or been given notice of the end of their employment

- a worker where the employer has reasonable grounds to believe the worker is protected from tax charges on their pension savings under HMRC’s primary, enhanced, fixed or individual protection requirements (see paragraph 103)

- a worker who holds the office of a director of the employer (paragraph 32 explains what it means to hold office as a director)

- a worker who is a member (partner) of a Limited Liability partnership and is not treated for income tax purposes as being employed by that limited liability partnership under section 863A of the Income Tax (Trading and other Income) Act 2005 (HMRC’s salaried members rules)

- a worker who has been paid a winding up lump sum payment (see paragraphs 112 to 118) whilst in the employment of the employer, and during the 12 month period that started on the date the payment was made, the worker:

- ceased employment with the employer after the payment has been paid, and

- was subsequently re-employed by the same employer

- a worker who meets the definition of a ‘qualifying person’ for the purposes of separate UK legislation on occupational pension schemes and cross-border activities within the European Union (but see paragraphs 119 and 120).

- The modification of the employer duties varies according to the exception that applies. In some circumstances the employer is given the choice whether to comply with a duty or not, while in other circumstances the duty is removed altogether. It is also possible for a worker to meet the conditions for more than one exception at the same time.

Ceasing active membership of a qualifying scheme

- A worker may already be an active member of a qualifying scheme on the employer’s duties start date as a result of contractual enrolment. On or after the duties start date, a worker may become an active member of a qualifying scheme as a result of automatic enrolment, opt in or automatic re-enrolment, or because the employer has chosen to use or continue to use contractual enrolment instead.

- A worker who is an active member of a qualifying scheme may choose to cease that active membership at any point either through opting out in the opt-out period or by ceasing active membership under the scheme rules. At the point that they cease active membership they may no longer be an eligible jobholder or even a jobholder.

- This exception applies to a worker who has ceased active membership, at their own request, of:

- a qualifying pension scheme (whether that be by opting out or under the scheme rules), or

- a pension scheme that would have been a qualifying scheme if they had been a jobholder.

- In other words it applies in relation to a worker who opted out or ceased active membership of a scheme which met the qualifying criteria for them, irrespective of what category of worker they were on the day membership ceased.

- Where this exception applies, the automatic enrolment and automatic re-enrolment duties are modified. All the other duties and safeguards continue to apply as usual. For more information on automatic re-enrolment see Detailed guidance no.11 – Automatic re-enrolment.

- The exception means the duty to automatically enrol does not apply in respect of any eligible jobholder who has previously opted out or ceased active membership more than12 months beforehand.

- Where a worker becomes an eligible jobholder within the 12 month period starting on the date that their active membership ceased at their request, then the automatic enrolment duty to that worker becomes optional. The employer can choose to automatically enrol the eligible jobholder if they wish, but they are not required to.

- Similarly where the employer’s automatic re-enrolment date falls within the 12 month period starting on the date active membership ceased at the worker’s request, then the employer can also choose whether to apply the automatic re-enrolment duty to that worker or not.

Leaving employment

- When a worker wishes to resign their employment (including on retirement) they must give their employer notice of their intent. And where an employer wishes to dismiss a worker from their employment they must give the worker notice of their intent. This exception applies in either scenario.

- The exception does not apply where the worker is at risk of dismissal or redundancy but notice of the end of employment has not actually been given. Nor does it apply to workers who are on fixed-term contracts, including short term contract workers, as their employment comes to an end on the expiry of the fixed term, rather than by notice to terminate an otherwise ongoing employment relationship.

- Where this exception applies, the automatic enrolment, automatic re-enrolment, opt- in and joining duties are all modified:

- the automatic enrolment duty becomes optional – the employer can choose to automatically enrol the worker but is not required to

- the automatic re-enrolment duty becomes optional – the employer can choose to automatically re-enrol the worker but is not required to

- if the employer is given a joining notice, they are not required to make arrangements to create active membership of a pension scheme

- The information duty and safeguards continue to apply as usual throughout the notice period.

- If notice is withdrawn these modifications fall away and the full employer duties start to apply again in relation to the worker and an immediate re-enrolment duty is triggered. See Detailed guidance no.11 – Automatic re-enrolment for more information.

Primary, Enhanced, Fixed or Individual tax protection on pension savings

- A worker who has built up pension savings above the Lifetime Allowance for HMRC purposes is protected from tax charges on those savings under HMRC’s primary, enhanced, fixed or individual protection requirements.

- Under these provisions a worker may have:

- Primary protection

- Enhanced protection

- Fixed protection 2012

- Fixed protection 2014

- Fixed protection 2016

- Individual protection 2014, or

- Individual protection 2016

This exception applies where an employer has reasonable grounds to believe that a worker has one of these protections from tax charges on their pension savings.

- In the regulator’s view, ‘having reasonable grounds to believe’ means that the employer must actually believe that the worker has the protection, and there must be evidence which would lead a reasonable person to believe this. Workers have to apply to HMRC for these protections and so will have documentation from HMRC detailing the type of protection from tax charges they have. Sight of a copy of the certificate issued by HMRC to the worker for example would be one way of giving the employer reasonable grounds to believe that the relevant protection applied, as would documented confirmation from the worker that they have this protection. Other evidence from the worker may also be sufficient.

- Where this exception applies, the employer can choose whether to apply the automatic enrolment duty or automatic re-enrolment duty to that worker in the event either duty is triggered but is not required to. All the other duties and safeguards continue to apply as usual.

Directors

- This exception applies to a worker who holds the office of director with the employer. Paragraph 32 explains what it means to hold office as a director.

- Where this exception applies, the employer can choose whether to apply the automatic enrolment duty or automatic re-enrolment duty to that worker in the event either duty is triggered but is not required to. All the other duties and safeguards continue to apply as usual.

- Employers should note the interaction with the exemption from the definition of worker described at paragraphs 29 to 32. Their first step will be to determine whether the director falls within the definition of a worker. It is only if they do that this exception to the automatic enrolment and automatic re-enrolment duties applies.

Partners in Limited Liability Partnerships

- In 2014 the Supreme Court ruled in Clyde & Co v Bates van Winklehof that a partner in a Limited Liability Partnership (LLP) was a worker under the Employment Rights Act 1996 (the ERA), in the particular circumstances of the case.

- Given the similarity in the definition of worker in the ERA and the Pensions Act 2008, the regulator’s view is that an LLP should assume that the Supreme Court’s decision is equally applicable to the Pensions Act 2008 for automatic enrolment purposes.

- The effect of this is not that every partner in an LLP is necessarily a worker for automatic enrolment purposes, rather that they could be a worker for those purposes.

- This exception applies to an LLP partner who satisfies the conditions to be a worker employed by the LLP, but who is not treated for income tax purposes as being employed by LLP under section 863A of the Income Tax (Trading and other Income) Act 2005. In other words, the partner is not treated by HMRC as a ‘salaried member’.

- Where this exception applies, the employer can choose whether to apply the automatic enrolment duty or automatic re-enrolment duty to the worker in the event either duty is triggered but is not required to. All the other duties and safeguards continue to apply as usual.

Winding-up lump sum payments

- Under HMRC provisions the trustees of defined contribution (DC) occupational pension schemes in wind-up are allowed to commute sums of under £18,000 provided certain conditions are met. One of these conditions for members below retirement age is that the employer gives an undertaking to HMRC not to contribute to a registered pension scheme for 12 months after the commuted payment is taken in respect of the worker who has been paid the commuted sum. The payment of this commuted sum is known as a ‘winding-up lump sum payment’).

- This exception applies where a worker has:

- been paid a winding- up lump sum payment whilst in the employment of the employer, and

- during the 12 month period starting on the date the winding up lump sum was paid, they:

- ceased employment with the employer and

- were subsequently re-employed by the same employer.

- Where this exception applies the automatic enrolment, re-enrolment, opt in, joining and information duties are all modified:

- the automatic enrolment duty does not apply in relation to a worker who was paid the winding-up lump sum payment more than 12 months before they meet the eligible jobholder criteria provided that they ceased employment and were re-employed during the 12 month period starting on the date the winding up lump sum was paid

- the automatic enrolment duty becomes optional in relation to a worker who meets the eligible jobholder criteria within the 12 month period starting on the date the winding up lump sum was paid

- the automatic re-enrolment duty becomes optional in relation to a worker who meets the eligible jobholder criteria within the 12 month period starting on the date the winding-up lump sum was paid

- the opt in duty does not apply in relation to a worker during the 12 month period starting on the date the winding-up lump sum was paid

- the joining duty does not apply in relation to a worker during the 12 month period starting on the date the winding-up lump sum was paid

- the requirement to give information about the right of a jobholder to opt in to an automatic enrolment scheme and the right of an entitled worker to join a pension scheme does not apply in relation to a worker during the 12 month period starting on the date the winding-up lump sum was paid. For more information on the different information requirements see Detailed guidance no. 10 – Information to workers.

- The automatic re-enrolment duty, opt in, joining and the information duties apply as usual from the end of the 12 month period that started on the date the winding up lump sum was paid. The safeguards continue to apply as usual throughout the 12 month period and after the end of the period.

- Employers should note that these modifications only apply where the worker has been paid the winding-up lump sum whilst in their employment and they have subsequently ceased employment and been re-employed by the same employer during the 12 month period starting on the date the winding up lump sum was paid. All the employer duties and safeguards continue to apply as usual where the worker has continued to be employed by the employer who gave the undertaking, or if the automatic enrolment date falls after the payment was made but before employment ceased.

- Offering the option of a winding-up lump sum is not obligatory. An employer should consider their obligations under the employer duties and whether they are in a position to give the required undertaking to HMRC. Relevant to their considerations are the following:

- the employer’s duties start date and whether this is more than 12 months away from the point of giving the undertaking (if postponement is used then that needs to be taken into account)

- the workers to whom a winding-up lump sum payment is being offered, for example: whether they are likely to meet the eligible jobholder criteria on or after the duties start date or at any time within the 12 month period of the undertaking to HMRC

- If the conclusion from consideration of the matters above is that the worker is likely to have to be automatically enrolled by the same employer during the 12 month period of the undertaking to HMRC, the employer is unlikely to be in a position to give the required undertaking.

‘Qualifying person’ for cross border legislation

- The UK legislation on cross border occupational pensions schemes was revoked on 31 December 2020. Although the corresponding exemption in the AE legislation in respect of a 'qualifying person' (as defined in the cross border requirements) was not amended at that time, in our view the exemption is no longer of any effect given that the underlying legislation has been revoked. This means that there are no longer statutory definitions of "qualifying person" or "European employer", to which the exemption refers.

- Since 1 January 2021 therefore an employer will no longer be exempt from their AE duties in respect of a worker who previously met the definition of 'qualifying person' in the cross border regulations. The conditions for one of the other exceptions may be met separately.

Keep track of age and earnings

- Changes in age and earnings may see a worker move between the different categories of worker. The employer duties in relation to that worker will therefore change. For this reason, it is important to monitor age and earnings – this is especially important for workers who earn below the qualifying earnings threshold, or who are under 22 years old.

- An employer will need to put procedures in place to monitor when their workers move from one category of worker to another, and alert them as to what this means in practice.

Examples of monitoring age and earnings

Reaching age 22

Simon is aged 20. He earns more than the earnings trigger for automatic enrolment. His employer does not need to automatically enrol him because he is not yet 22 years old. However, Simon can choose to opt in to the scheme. His employer will need to give him information about both the right of a jobholder to opt in and the right of an entitled worker to join.

The employer will also need to keep track of Simon’s age because, on his 22nd birthday, Simon will then need to be automatically enrolled as he will become an eligible jobholder (assuming he still has earnings above the earnings trigger for automatic enrolment).

Earning qualifying earnings

Jasmine is 27 years old and works part time in her local shop. Her employer does not need to automatically enrol her because her earnings are below the lower level of qualifying earnings. However, Jasmine is an entitled worker so her employer will need to give her information about both the right of a jobholder to opt in and the right of an entitled worker to join.

When her children start school, Jasmine starts working more hours, which pushes her earnings above the earnings trigger for automatic enrolment. Jasmine’s employer must now automatically enrol her, as she has become an eligible jobholder.

What next?

All employers should find out if they are subject to the new employer duties and, if affected, when these duties will apply to them. Detailed guidance no. 2 – Getting ready provides more information on the steps an employer can take to prepare for automatic enrolment.

Further information to help employers comply with the new duties and safeguards can be found in other guidance in this series.

Employers should identify if they are subject to the duties

Key terms

Summary of the different categories of worker

| Category of worker | Description of worker |

|---|---|

| Worker | An employee or someone who has a contract to perform work or services personally, that is not undertaking the work as part of their own business. |

| Jobholder |

A worker who:

|

| Eligible jobholder |

A jobholder who:

|

| Non-eligible jobholder |

A jobholder who:

|

| Entitled worker |

A worker who:

|