Pension schemes under the employer duties

Automatic enrolment detailed guidance for employers no. 4

Accompanying resources

Information to workers

Summary of information requirements in a quick-reference table format

The different types of worker

Diagram of the different categories of worker and the criteria for each category

Employer duties and safeguards

At-a-glance summary of the duties and safeguards

Please note: This guidance is linked to the following appendices

- Appendix A (full-page figure (opens in new tab)): Steps to take to determine if your DB pension scheme is a qualifying scheme

- Appendix B - occupational (full-page figure (opens in new tab)): Steps to take to determine if your DC pension scheme is a qualifying scheme

- Appendix B - personal (full-page figure (opens in new tab)): Steps to take to determine if your DC pension scheme is a qualifying scheme

- Appendix C: The relevant pay reference period for the purposes of the minimum contribution entitlement

- Appendix D: Entitlement check for DC occupational and personal pension schemes

How to save this page as a PDF

About this guidance

This guidance is aimed at professional advisers and employers with in-house pensions professionals. Trustees, managers and providers of pension schemes will also find it useful.

It provides factual information on the required criteria for a pension scheme to be an automatic enrolment scheme and/or a qualifying scheme, as set out in legislation. This includes the requirements for both UK and non-UK pension schemes.

Employers reading this guidance should already understand whether they need an automatic enrolment scheme, a qualifying scheme, or a combination of the two, to meet their duties. In order to understand this, employers should first read:

- Detailed guidance no. 1 – Employer duties and defining the workforce

- Detailed guidance no. 2 – Getting ready

We recognise that many employers will already have pension provision for their workers, and that this will often match or exceed the minimum requirements contained in the duties. In these cases, such employers may just need to check that the minimum requirements are covered in their existing processes.

There are certain terms used in this guidance that are explained further in other guidance in this series, specifically Detailed guidance no. 5 – Automatic enrolment and Detailed guidance no. 6 – Opting in, joining and contractual enrolment. It may be useful to have them to hand as a point of reference when reading this guidance.

It will help employers if they are familiar with the different categories of workers. These are explained in Detailed guidance no. 1 – Employer duties and defining the workforce. A quick reminder is also available in Key terms.

This guidance forms part of the latest version of the detailed guidance for employers (published June 2021).

Changes from last version

- qualifying earnings thresholds have been updated for the 2021/22 tax year

- changes to the automatic enrolment criteria for non-UK pension schemes following the UK’s exit from the EU have been added

- out of date content relating to an employer’s staging date and the statutory increases in the minimum contribution requirement in 2018 and 2019 have been removed

Paragraph numbers have changed as a result of these amendments.

Employers need to be familiar with the different categories of workers

Introduction: Automatic enrolment and qualifying pension schemes

- The employer duties require employers to put certain jobholders into a pension scheme. An employer must:

- automatically enrol any eligible jobholders into an automatic enrolment scheme, unless they are already an active member of a qualifying scheme with that employer

- enrol any non-eligible jobholders who give the employer an opt-in notice into an automatic enrolment scheme, unless they are already an active member of a qualifying scheme with that employer.

- An employer who is putting a pension scheme in place for the first time to fulfil their enrolment duties, will need to put an automatic enrolment scheme in place with effect from the date one of the duties above first apply to them.

- An employer will need to understand what makes a pension scheme an automatic enrolment scheme, and what makes it a qualifying scheme.

- This guidance describes the required criteria. The guidance is divided into five sections:

- an overview of automatic enrolment and qualifying schemes

- the automatic enrolment criteria for UK and non-UK pension schemes, and what the criteria mean in practice

- the qualifying criteria for UK and non-UK pension schemes

- the minimum requirements for UK and non-UK pension schemes by scheme type

- what the qualifying criteria and minimum requirements mean in practice.

- When choosing a pension scheme to fulfil their duties, an employer might use an existing pension scheme or set up a new occupational or personal pension scheme.

- Whether it is a new or existing pension scheme, an employer must be satisfied that it meets the criteria to be an automatic enrolment scheme or to be a qualifying scheme before they can use it.

- It is important to note that these criteria are the minimum features the pension scheme is required to have. There will be other things to consider before an employer makes a decision about what type of pension scheme to use.

- Some employers will pay for professional advice while others will make decisions with information from a range of sources. We support employers in understanding the process for selecting a pension scheme for automatic enrolment.

- Further information for employers to help them understand the factors they should consider when choosing a pension scheme.

Location of the pension scheme

- The location of the main administration of the pension scheme is a relevant consideration when an employer is considering their options.

- A pension scheme whose main administration is in the UK can be used for automatic enrolment and can also be used as a qualifying scheme, provided it meets the relevant criteria.

- A pension scheme whose main administration is in a country outside the UK cannot be used for automatic enrolment. It can be a qualifying scheme, provided it meets the relevant criteria, and so may be used for existing members of the pension scheme.

Overview of automatic enrolment and qualifying schemes

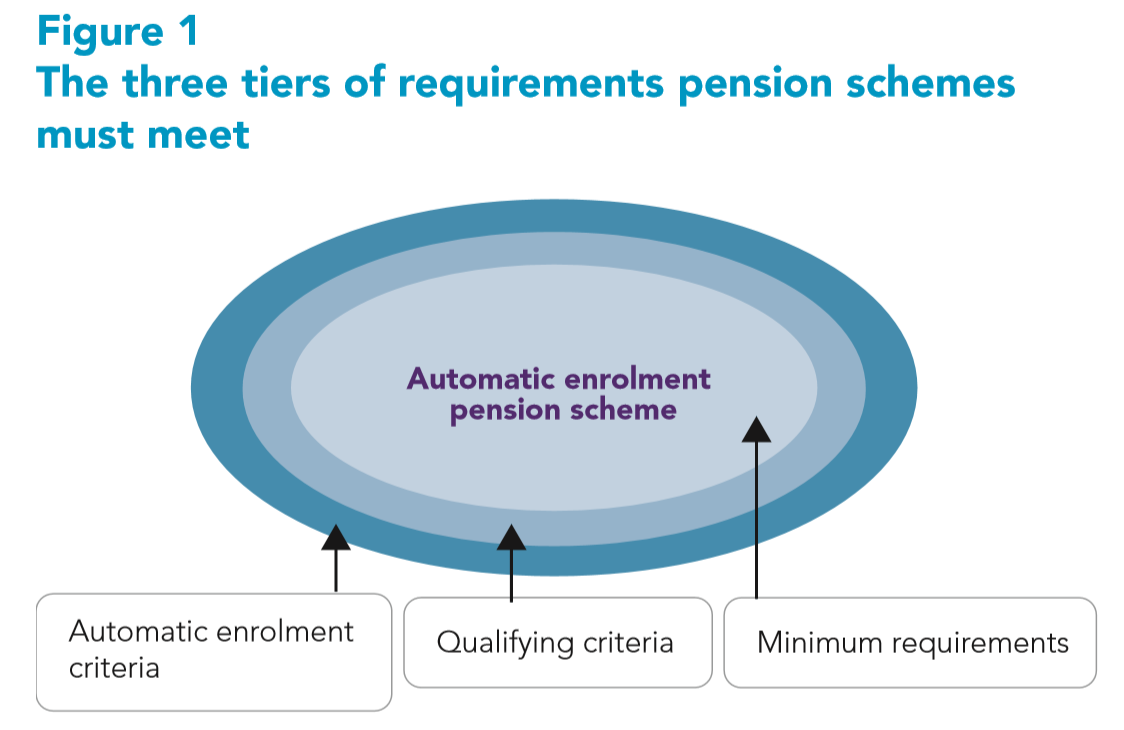

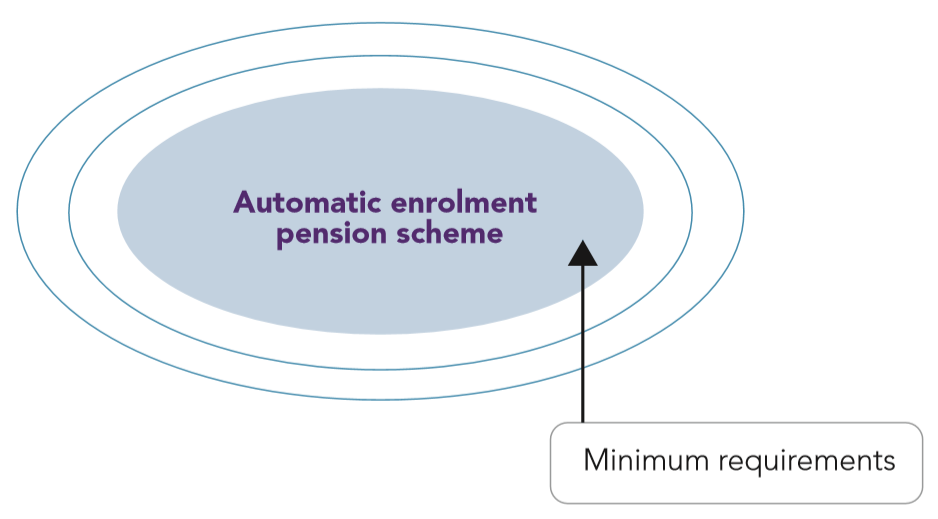

- There are three tiers of requirements that a pension scheme must meet in order to be an automatic enrolment scheme. Figure 1 illustrates these tiers.

- An automatic enrolment scheme must meet the automatic enrolment criteria, the qualifying criteria and the minimum requirements. An employer must ensure that their pension scheme meets the criteria to be an automatic enrolment scheme if they want to use it for automatic enrolment, or for enrolling any jobholders who have opted in.

- The minimum requirements differ depending on the type of pension scheme (eg whether the scheme is a DC or DB pension scheme). The minimum requirements are described in the section of this guidance entitled Minimum requirements by pension scheme type.

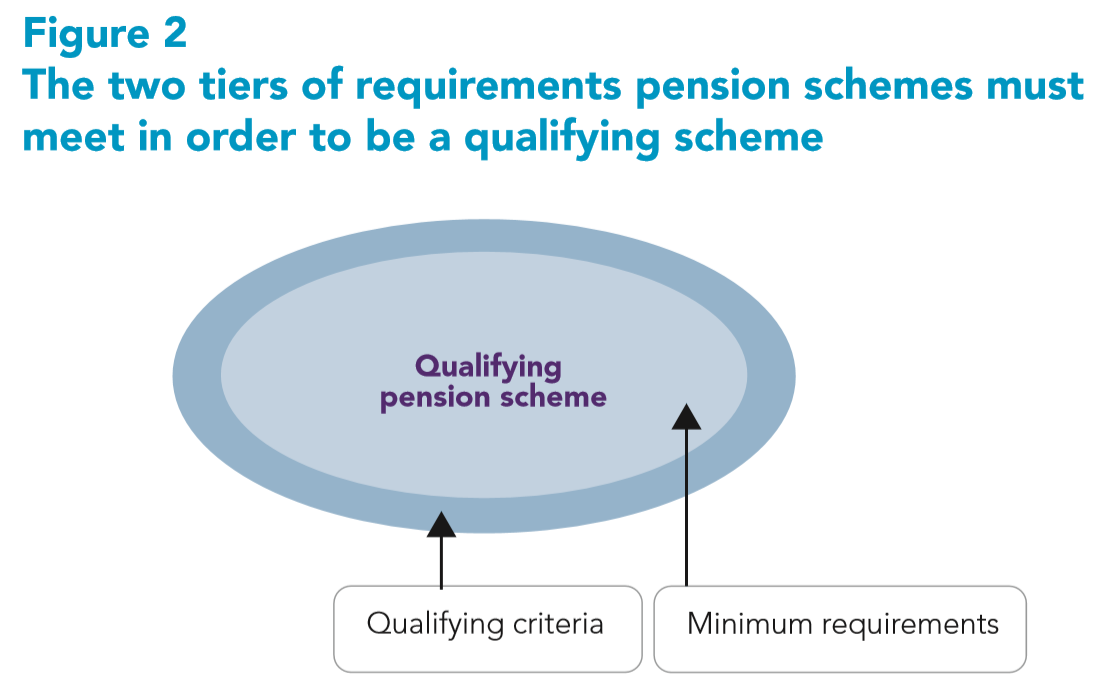

- There are two tiers of requirements that a pension scheme must meet in order to be a qualifying scheme. Figure 2 illustrates these tiers.

- A qualifying scheme must meet the qualifying criteria and the minimum requirements.

In summary

- A qualifying scheme is a scheme that meets certain minimum requirements with some additional conditions (the ‘qualifying criteria’). These are described in the section of this guidance entitled Qualifying criteria.

- An automatic enrolment scheme is a qualifying scheme with some additional features (the ‘automatic enrolment criteria’) which means the employer can use it for automatic enrolment. These additional features are described in the section of this guidance entitled Automatic enrolment criteria. Broadly, this means that there should be nothing in the rules of the pension scheme which would act as a barrier to automatic enrolment.

Automatic enrolment criteria

- An employer must ensure that their pension scheme meets the criteria (set out below) if they want to use it for automatic enrolment, or for enrolling any jobholders who have opted in.

- To be an automatic enrolment scheme, a scheme must meet the qualifying criteria (set out in the next section) and in addition, it must not contain any provisions that:

- prevent the employer from making the required arrangements to automatically enrol, opt in or re-enrol a jobholder

- require the jobholder to express a choice in relation to any matter, or to provide any information, in order to remain an active member of the pension scheme

- If the scheme is a money purchase scheme, it must also not contain any provisions that allow either:

- an amount to be deducted from a jobholder’s pension pot or contributions, or

- the value of a jobholder’s pension rights to be reduced by any amount,

- if that amount is to be paid to a third party under an agreement with the employer unless the third party is either the member, the scheme trustee/manager, or the scheme provider. This is colloquially known as a ‘consultancy charge’.

- Pension schemes with their main administration outside the UK cannot be used for automatic enrolment.

What the automatic enrolment criteria mean in practice

- Practically, the automatic enrolment criteria mean that the rules of the pension scheme cannot:

- contain any barrier to enrolment into the pension scheme, eg if a scheme has an age restriction of 21, the employer may use it for automatic enrolment but will need to change the scheme rules or provide another automatic enrolment scheme for any jobholders under 21 who wish to opt in

- require a jobholder to provide information to become or remain a member, eg to complete an application form or give consent

- require an employer to provide information about the jobholder as a condition of joining beyond the specified information required for automatic enrolment, unless the employer is satisfied that they will be able to provide this information within a period of time short enough to not hamper the automatic enrolment process

- require a jobholder to make any choice to join or remain a member of a pension scheme, eg to make any choice about the fund their contributions will be invested in before they can become a member. However, the jobholder may express a choice voluntarily, if they wish, and if the scheme rules allow for it. An automatic enrolment scheme will therefore have to provide a default fund for all jobholders who do not express an opinion or choice. The Department for Work and Pensions (DWP) has published default guidance setting out industry standards for governance of funds, charging structure and communications. This guidance can be viewed at automatic enrolment in workplace pensions.

- If an employer has to pay for advice regarding a money purchase scheme that they intend to use for automatic enrolment, then they will no longer be able to enter into an agreement to deduct such charges from the jobholder’s contributions or entitlement under the scheme.

Qualifying criteria

- All automatic enrolment schemes must also meet the qualifying criteria. Any existing pension scheme that the employer already provides before their duties start date will also have to meet the qualifying criteria, if the employer wants to continue to use it for those workers that are already active members.

- A qualifying scheme may be a UK scheme (one with its main administration in the UK) or a non-UK scheme (with its main administration outside the UK).

- For a UK pension scheme to be qualifying in relation to a jobholder, it must:

- be an occupational or personal pension scheme

- be tax registered, and

- satisfy certain minimum requirements. (The requirements differ according to the type of pension scheme and are described in the section of this guidance entitled Minimum requirements by pension scheme type.)

- For a non-UK pension scheme to be qualifying in relation to a jobholder, it must:

- be an occupational pension scheme (note 1) and, in the country where it has its main administration, there must be a body that regulates occupational pension schemes and that scheme itself, or

- be a personal pension scheme (note 2) and, in the country where it is established, there must be a body that regulates personal pension schemes and the provider of that scheme, and

- satisfy the condition that the regulatory requirements provide that some of the benefits may be used to provide the jobholder with an income for life.

- In addition, the non-UK pension scheme must:

- meet one of the following criteria:

- It is a qualifying overseas pension scheme (QOPS), or

- Jobholders receive tax relief on their contributions because of a double taxation agreement, or

- Jobholders receive tax relief on their contributions under chapter 2, part 5 of the Income Tax (Earnings and Pensions) Act 2003 in accordance with paragraph 51 of Schedule 36 of the Finance Act 2004, or

- It is a money purchase pension scheme whose jobholders do not receive any tax relief on their contributions but the employer’s contribution includes an additional amount, which is equivalent in value to the tax relief that jobholders would have received, had the pension scheme been tax registered in the UK, and

- satisfy the same minimum requirements as for UK pension schemes, as set out in the section of this guidance entitled Minimum requirements by pension scheme type

- meet one of the following criteria:

Notes on Qualifying criteria

- [1] Occupational pension scheme (non-UK) is:

- an institution for occupational retirement provision (IORP) that has its main administration in a non-UK state, or

- a pension scheme that has its main administration outside the UK, and meets the definition of an occupational pension scheme as set out in section 1(1) of the Pension Schemes Act 1993.

- [2] Personal pension scheme (non-UK)

- Outside the UK a personal pension scheme must be:

- regulated by a competent authority, and

- carried on by a person who is in relation to that activity authorised by a competent authority

Minimum requirements by pension scheme type

- These minimum requirements differ according to the type of pension scheme. They apply to both UK pension schemes and non-UK pension schemes, except where indicated. An employer need only consider the minimum requirements that are relevant to their pension scheme type.

- The minimum requirements for DC pension schemes, and DB schemes that satisfy certain conditions, set a minimum contributions entitlement. There are some additional requirements where the DC pension scheme is a contract-based scheme (ie a personal pension). For employers who provide a DC pension scheme, there is an alternative way of meeting the requirements called ‘certification’.

- The minimum requirements for DC pension schemes (and DB schemes that satisfy certain conditions) including certification that the scheme meets the minimum requirements for money purchase schemes, are described in paragraphs 36-65.

- The minimum requirements for DB pension schemes set a benchmark for a jobholder’s entitlement to benefits, or for the cost of providing those benefits, and are described in paragraphs 66-82.

- The minimum requirements for hybrid pension schemes (a scheme which is neither only a DB nor only a DC, but which generally has elements of both) are described in paragraphs 83-86.

DC occupational pension schemes

- The minimum requirements for DC occupational pension schemes, and DB schemes that satisfy certain conditions, are based on the contribution rate and require that under the scheme:

- the employer must make contributions in respect of the jobholder

- a total minimum contribution, however calculated, must be at least 8% of the jobholder’s qualifying earnings (see paragraph 38) in the relevant pay reference period (note 3)

- a minimum employer’s contribution, however calculated, must be at least 3% of the jobholder’s qualifying earnings in the relevant pay reference period.

- ‘Under the scheme’ means under the rules of the pension scheme or other binding agreement with the employer.

- ‘Qualifying earnings’ is a reference to earnings of between £6,240 and £50,270 9 (note 4) made up of any of the following components of pay (‘earnings’) that are due to be paid to the worker:

- salary

- wages

- commission

- bonuses

- overtime

- statutory sick pay

- statutory maternity pay

- ordinary or additional statutory paternity pay

- statutory adoption pay.

- The assessment of whether a component of pay constitutes an element of qualifying earnings is for the employer to make. It is a separate and distinct assessment to deciding what constitutes basic pay for the purposes of a pension scheme that is using certification to meet minimum requirements as part of the qualifying criteria.

Notes on DC occupational pension schemes

- [3] See Appendix C for further information on the relevant pay reference period.

- [4] These figures are for the 2023 to 2024 tax year. The DWP reviews them every year, and any changes will be published on our website in advance of the new thresholds becoming effective.

DC personal pension schemes

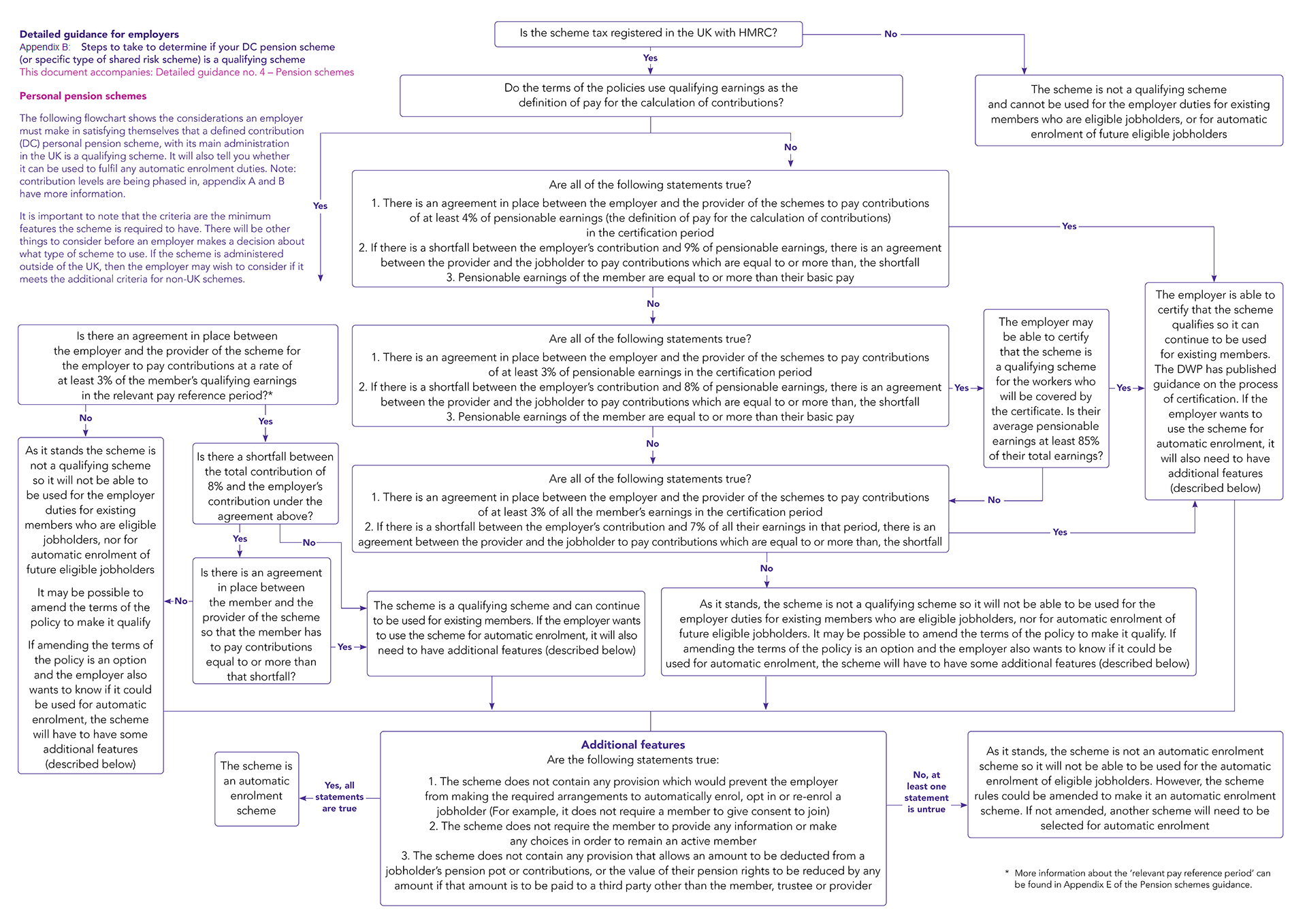

- The minimum requirements for personal pension schemes are also based on the contribution rate but, in addition, include requirements governing the mechanism for paying those contributions and the type of pension benefit provided.

- Therefore, to be a qualifying scheme, a personal pension scheme must:

- be subject to regulation by the Financial Conduct Authority (FCA) – except in the case of a personal pension scheme whose main administration is outside the UK – and

- have its operations carried out in the UK by a person who is an authorised person or an exempt person under section 19 of the Financial Services and Markets Act 2000, and

- provide money purchase benefits – except in the case of a personal pension scheme whose main administration is outside the UK – and

- have certain types of agreements in place between the employer, the jobholder and the provider of the personal pension scheme.

- The agreements are as follows:

A. Agreement between the provider of the pension scheme and the employer

- There must be an agreement between the provider of the pension scheme and the employer under which:

- the employer must make contributions in respect of the jobholder, and

- the employer’s contribution, however calculated, must be at least 3% of the jobholder’s qualifying earnings in the relevant pay reference period (set out in Appendix C).

- We expect the agreement to create a legally binding obligation (preferably by means of a written contract) on the employer to pay minimum contributions in respect of the jobholder to the provider of the pension scheme. It is unlikely that an existing group personal pension scheme or stakeholder pension scheme will have such an agreement in place.

B. Agreement between the provider of the pension scheme and the jobholder

- This agreement is only needed if the employer’s contribution is less than 8% of the jobholder’s qualifying earnings and the jobholder is therefore required to make contributions.

- Where this is the case, there must be an agreement between the provider of the pension scheme and the jobholder, under which:

- the jobholder must make contributions which, however calculated, are at least equal to the difference between:

- 8% of the jobholder’s qualifying earnings in the relevant pay reference period (set out in Appendix C), and

- the employer’s contribution under the agreement in (A) above.

The jobholder can choose to pay more than any shortfall if they wish.

- It is for the provider of the pension scheme to decide how to put in place this agreement, but we think that it may form part of the terms and conditions issued to the jobholder.

C. Direct payment arrangements

- There must be direct payment arrangements between the employer and the jobholder. Direct payment arrangements are arrangements under which the employer (or someone acting on their behalf) pays contributions to the pension scheme. The contributions are either:

- on the employer’s own account but in respect of the jobholder (ie employer contributions), or

- on behalf of the jobholder (jobholder contributions if the jobholder is making any) out of deductions from the jobholder’s pay.

- The direct payment arrangements must set out the due dates for paying these contributions.

- Jobholder contributions deducted from pay must be paid to the pension scheme by the 19th day of the month following deduction (or 22nd day if the payment is by electronic means). There are special rules for the first deductions after joining. For more information see Detailed guidance no. 5 – Automatic enrolment.

- Employer contributions must be paid by the latest date set out under the arrangements for paying them to the pension scheme.

- Direct payment arrangements are not required to be a written agreement on a single document. Essentially, direct payment arrangements exist where:

- the employer makes employer contributions to a personal pension scheme (as is required under agreement (A)), or

- the employer deducts the jobholder’s contributions from pay and pays them across to the pension scheme for the jobholder, or

- the employer does both.

- A combination of other written and verbal agreements may exist between the provider of the pension scheme, the employer and the jobholder that constitute direct payment arrangements. In fact, because as part of the minimum requirements, there must be an agreement between the provider of the pension scheme and the employer under which the employer must make contributions, this will likely constitute evidence of the direct payment arrangements.

Certification

- Existing DC pension schemes, whether occupational or personal pension schemes, will base contributions on percentage rates of pensionable pay. The definition of pensionable pay in the scheme rules is likely to be different to qualifying earnings. Pensionable pay may just include basic pay and not overtime or bonuses and may require contributions to be deducted from the first pound earned, or from a band of earnings different to qualifying earnings.

- In recognition of this, employers with DC schemes or DB schemes that satisfy certain conditions are able to self-certify that their scheme meets the minimum requirements. One way of doing this is for employers to certify their scheme with respect to one of the alternative DC requirements. These requirements comprise three sets as follows:

- Set 1: A total minimum contribution of at least 9% of pensionable pay (at least 4% of which must be the employer’s contribution), or

- Set 2: A total minimum contribution of at least 8% of pensionable pay (at least 3% of which must be the employer’s contribution), provided that pensionable pay constitutes at least 85% of earnings (the ratio of pensionable pay to earnings can be calculated as an average at scheme level), or

- Set 3: A total minimum contribution of at least 7% of earnings (at least 3% of which must be the employer’s contribution) provided that all earnings are pensionable.

- To certify, the rules of the scheme must require contributions in line with one of the sets. Where a personal pension is used, similar agreements to those described in paragraphs 46 to 50 between the scheme, jobholder and employer must be in place which reflect the contribution levels in one of the sets.

- ‘Earnings’ has the same meaning as in section 13(3) of the Pensions Act 2008 (see paragraph 38 for more information).

- For sets one and two, pensionable pay must be at least equivalent to basic pay. Basic pay is defined as the gross earnings (see paragraph 59) of the jobholder, disregarding the gross amount of:

- any commission, bonuses, overtime or similar payments

- any shift premium pay, and

- any reasonable allowance with respect to:

- any duty of the jobholder, such as a duty in connection with the role of fire or bomb warden, that is ancillary to the main duties of the jobholder’s employment

- the cost of relocation of the jobholder to a different place of work

- in a case not covered by ii), the purchase, lease or maintenance of a vehicle

- in a case not covered by ii) or iii), the purchase, lease or maintenance of an item, or

- in a case not covered by ii), iii) or iv), the delivery of a service to the jobholder.

- This definition of basic pay is separate to the assessment of what components of pay make up qualifying earnings. Qualifying earnings are described in paragraph 38. When an employer is assessing their worker to identify which category of worker they fall into, they must assess whether qualifying earnings are payable in the relevant pay reference period. This is explained in Detailed guidance no. 3 – Assessing the workforce.

- Some employers may be unable to, or not wish to, certify that their scheme meets one of the alternative DC requirements because, for example, elements of non-pensionable pay are fluctuating. These employers may instead wish to certify that their scheme meets the minimum requirements in the Act. They can do this if an examination of current remuneration data for all relevant jobholders reveals that their entitlement under the scheme has met the minimum requirements in practice.

- The employer has one month from the effective date of the certificate (which, for the first certificate, will usually be the scheme’s duties start date) to carry out any necessary checks and calculations and sign the certificate. They may look forward for up to 18 months (the maximum certification period) to certify that their scheme will be qualifying for that period. At the end of the period, if the employer wishes to re-certify, they must do so within one month.

- The DWP has practical guidance for employers and their advisers on the certification of DC schemes and the DC element of certain hybrid schemes: Automatic enrolment: guidance on certifying money purchase pension schemes (PDF, 322kb, 43 pages).

- An employer can also determine whether their scheme meets the minimum requirements by carrying out an entitlement check. Broadly, this entails carrying out an individual check for each worker to establish whether the worker’s entitlement under the scheme rules is at least equivalent to the minimum requirements for a DC scheme. Details on how to carry out an entitlement check are set out in Appendix D.

Additional requirements for qualifying DC schemes

- Even if a scheme meets the qualifying criteria, there are a number of additional requirements that must be met for a scheme to be used as a qualifying scheme by an employer. The duty to check that these requirements are met falls upon the trustees and managers of the scheme and not the employer. The requirements include:

- a limit on the charges that members pay out of their pension pot

- a ban on Active Member Discounts, where members who no longer contribute to the scheme pay higher charges than those members who currently contribute to the scheme

- a ban on commission charges, where scheme members cover commission costs paid to advisers by administration and service providers for advice given to employers or their staff.

- We provide more information about restrictions on costs and charges for trustees and managers of occupational pension schemes. Employers may also find this information useful as background to these requirements.

DB pension schemes

- The minimum requirements for DB pension schemes are usually based on the benefits to which a jobholder is entitled under the pension scheme at retirement or the cost of providing those benefits. However, schemes that satisfy certain conditions are allowed to meet the DC minimum requirements.

- Prior to the abolition of contracting out on 6 April 2016, many DB pension schemes satisfied the minimum requirements if the employer had been issued with a contracting-out certificate and all the jobholders were in contracted out employment. These schemes must now meet either the test scheme standard or one of the alternative DB requirements as set out below.

Test scheme standard

- The test scheme is a hypothetical scheme, which is used as a benchmark. A pension scheme will satisfy the test scheme standard if it provides benefits that are broadly equivalent to, or better than, the benefits the test scheme would provide.

- A pension scheme does not have to exactly match the structure of the test scheme to satisfy the test scheme standard, but the benefits provided must be broadly equivalent to, or better than those in the test scheme.

- The key features of the test scheme include:

- entitlement to a pension from age 65, gradually increasing to 68 (to reflect increases in state pension age) and continuing for life

- an annual pension of 1/120th (or a lump sum of 16% for final salary lump sum schemes) of average qualifying earnings in the three tax years before the end of pensionable service, multiplied by the number of years of pensionable service, up to a maximum of 40 years

- for average salary lump sum schemes:

- a lump sum of 16% of qualifying earnings averaged over pensionable service, multiplied by the number of years of pensionable service, up to a maximum of 40 years with revaluation in service by the annual increase in either the Retail Price Index (RPI) or the Consumer Price Index (CPI), capped at 2.5%, or

- a lump sum of 8% of qualifying earnings averaged over pensionable service, multiplied by the number of years of pensionable service, up to a maximum of 40 years with revaluation in service by the annual increase in either the RPI or the CPI, capped at 2.5% plus a further 3.5% per annum and revaluation in deferment of 3.5% per annum in addition to that required by the bullet below

- revaluation of accrued benefits in deferment in accordance with section 84 of the Pension Schemes Act 1993

- annual increase of pensions in payment in accordance with section 51 of the Pensions Act 1995

- The comparison of a pension scheme’s benefits with those provided by the test scheme will usually be done by the scheme actuary.

- In some circumstances, the employer may self-certify that their pension scheme meets the standards of the test scheme, providing no actuarial calculations or comparisons are required. If the employer does self-certify, they can delegate calculations, if they prefer, but the employer remains responsible for ensuring the pension scheme meets the requirement.

- The DWP has issued guidance for employers and actuaries on the certification of qualifying schemes and the comparison to the test scheme, take a look at guidance for employers, trustees and advisers.

- Schemes that fail to satisfy the test scheme standard, cannot be qualifying schemes unless they meet one of the alternative DB requirements.

Alternative DB requirements

- On 1 April 2015, the government introduced two alternative tests for a DB scheme to satisfy the qualifying criteria. One is based on the cost to the scheme of the future accrual of active members’ benefits and the other is intended to allow DB schemes that satisfy certain conditions and that meet the minimum requirements for DC occupational schemes to be used for automatic enrolment.

Cost of accruals test

- The cost of accruals test is based on the cost of providing members’ benefits. It is applied at benefit scale level if the scheme has more than one scale of benefits and the actuary determines that there is a material difference in cost between the benefit scales. The period covered by the test is normally to be taken from the most recent written report signed by the actuary, or, in the absence of such a report, twelve months. Employers should therefore be able to rely upon any relevant actuarial work that has been carried out recently, for example, a funding valuation report.

- To satisfy the test, the cost of providing benefits in respect of each benefit scale must require a contribution rate of at least:

- 10% of qualifying earnings

- 11% of pensionable earnings provided those earnings are at least equivalent to basic pay (as defined in paragraph 57)

- 10% of pensionable earnings provided those earnings are at least equivalent to basic pay (as defined in paragraph 57) and the ratio of pensionable earnings to total pay averages out at least 85% over the scheme as a whole

- 9% of pensionable earnings provided all earnings are pensionable or

- 13% of pensionable earnings, provided those earnings are at least equivalent to the amount of basic pay (as defined in paragraph 65) that is above either the National Insurance (NI) lower earnings limit (see Appendix C) or the amount of the basic state pension.

- For schemes that do not provide survivors’ pension benefits, a contribution rate which is 1% less than the amounts set out in paragraph 77 is acceptable.

Money purchase minimum requirements

- DB schemes that satisfy certain conditions are permitted to meet the minimum requirements for DC occupational schemes (as set out in paragraphs 36-39 and 54-63 of this guide) in order to comply with the employer’s automatic enrolment duties.

- The DWP has issued guidance for pension professionals on the alternative DB requirements at alternative quality requirements for defined benefit and hybrid pension schemes.

Average salary pension schemes

- As well as meeting either one of the alternative DB requirements or being broadly equivalent to or better than the test scheme standard, average salary pension schemes must also meet certain additional criteria in respect of accrued benefits, in order to meet the minimum requirements.

- The additional criteria are that, during a jobholder’s pensionable service, any benefits that accrue to the jobholder must be revalued as follows:

- by the annual increase in either the RPI, or the CPI capped at 2.5% (the minimum rate) (note 5), or

- if either, under the scheme, accrued benefits are to be revalued at any time at less than the minimum rate, for example because revaluation is by the increase in average earnings rather than inflation, or there is a discretionary power in the scheme rules to revalue accrued benefits:

- the funding of the pension scheme must be based on the assumption that accrued benefits would be revalued at or above the minimum rate in the long term, and

- such funding must be provided for in the pension scheme’s statement of funding principles required under part 3 of the Pensions Act 2004, or in an equivalent funding statement if the pension scheme is not subject to the part 3 funding requirements of the Pensions Act 2004 (for example a non-UK pension scheme).

Note on Average salary pension schemes

[5] For a new public service average salary scheme, the minimum rate is an annual increase or decrease in either the percentage change in earnings or prices (depending on the scheme) as specified under s9(2) of the Public Service Pensions Act 2013 for the year by reference to which the revaluation is made.

Hybrid pension schemes

- A hybrid pension scheme is a scheme which is neither purely a DB nor purely a DC, but which generally has elements of both.

- Depending on the type of pension scheme, it will have to meet:

- the same minimum requirements as for DB pension schemes or a modified version, or

- the same minimum requirements as a DC pension scheme or a modified version, including the option to use the certification process, or

- a combination of the above

- Generally, each section of the scheme should be treated as if it is a separate scheme and the appropriate minimum requirements applied to each section. As long as one section meets the relevant minimum requirements, the scheme will qualify. However, there are some variations, as follows in Table 1.

Table 1: Minimum requirements for some types of hybrid pension scheme

| Types of hybrid scheme | Applicable minimum requirements |

|---|---|

| Sequential Both DB and DC benefits accrue in the scheme but not at the same time (eg members start in the DC section and move into the DB section after a specified number of years) |

Treat each section as a separate scheme, however, both sections must satisfy the relevant requirements |

| Self-annuitising Benefits accrue on a DC scheme but the pension is paid by the scheme, rather than each member’s pot being used to buy their pension |

Treat as a DC scheme |

| Combination Both DB and DC benefits accrue at the same time |

Treat each section as a separate scheme and if either section meets the relevant minimum requirements, the scheme will qualify. However, if neither section meets the minimum requirements in full, they may be applied proportionately in aggregate. |

- The DWP has practical guidance for employers and actuaries on how to certify that DB and hybrid schemes meet the appropriate minimum requirements: Guidance for employers on certifying defined benefit and hybrid pension schemes (PDF, 322kb, 52 pages).

What the qualifying criteria mean in practice

- An employer has to be satisfied that the pension scheme they are using to fulfil their duties meets the qualifying criteria. This is either as part of being satisfied that the pension scheme is an automatic enrolment scheme, or for checking that their existing pension scheme meets the qualifying criteria so they can continue to use it for existing members.

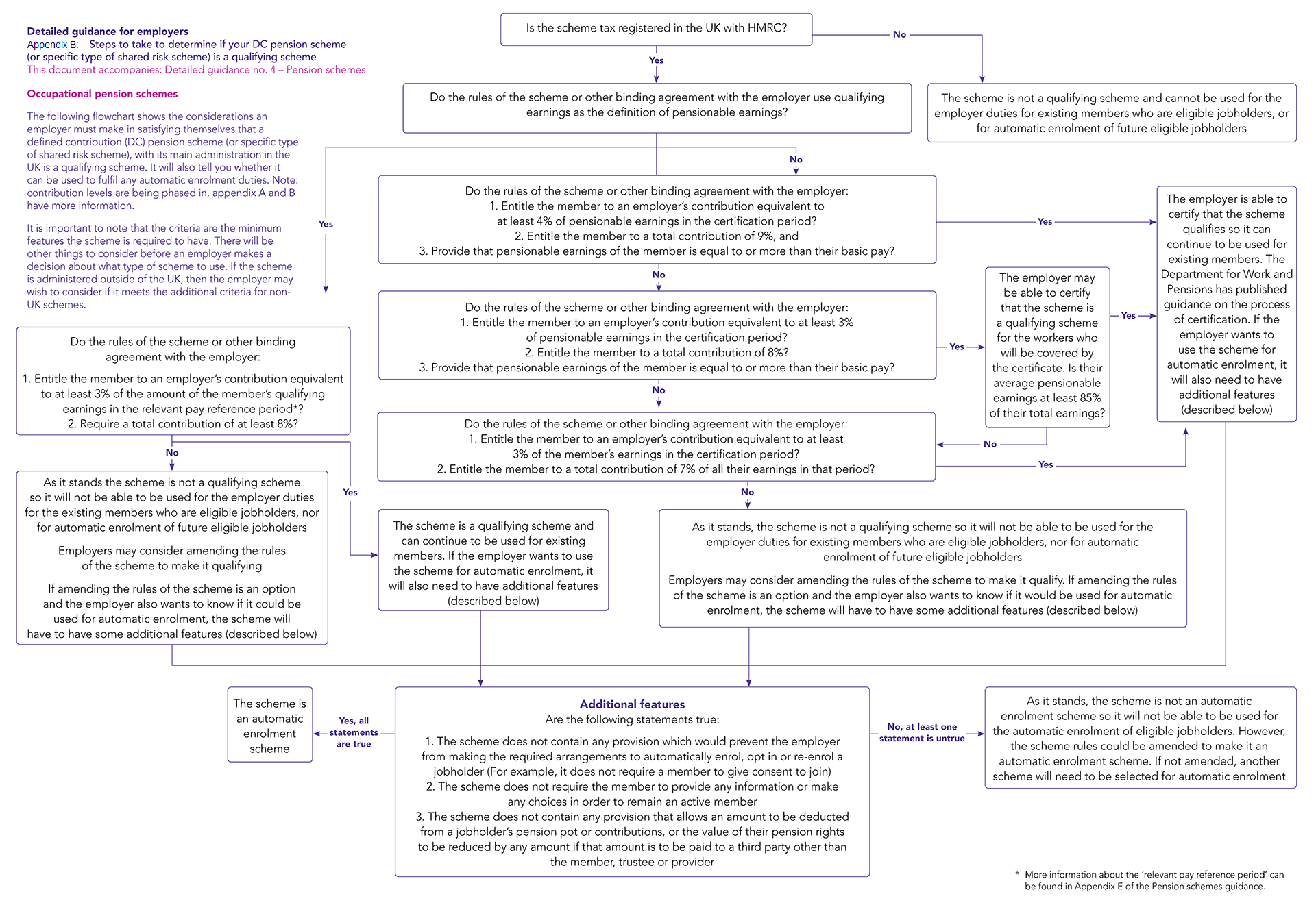

- For DB pension schemes or those hybrid pension schemes which have to meet the DB minimum criteria, this might be straightforward. Appendix A (full-page figure (opens in new tab)) has a flowchart showing the steps an employer may use in determining whether the qualifying criteria are met for a pension scheme with its main administration in the UK.

- For DC pension schemes, those hybrid pension schemes that must meet the DC minimum requirements, or DB schemes that meet certain conditions and are therefore allowed to qualify by meeting the DC minimum requirements, the employer will need to be satisfied that the entitlement under the rules of the pension scheme (or agreements in the case of personal pensions) is equivalent to, or better than, a total contribution of 8% of a jobholder’s qualifying earnings in the relevant pay reference period (see Appendix C).

An employer should check the rules of the scheme (or agreement)

- An employer should first check the rules of the scheme (or agreements). If they explicitly state that:

- the pension scheme requires, as a minimum, a total contribution of 8% of the jobholder’s qualifying earnings in the relevant pay reference period

- of which the employer’s contribution is at least 3%

the employer can then be satisfied that the pension scheme meets the minimum requirements.

- There is no requirement to check the amount of contributions that are actually paid for the purposes of establishing if the pension scheme meets the minimum requirements. However, an employer will still need to ensure that they are making the correct payments on time, as required by the pension scheme under the existing law on payment of contributions.

- Alternatively, the employer may choose to certify that the scheme meets one of the alternative DC requirements. They may do this if the rules of the scheme they want to use:

- require contributions to be deducted from the first pound earned, or on a band of earnings different to that used for qualifying earnings

- do not use qualifying earnings as the definition of pensionable pay, and

- have a definition of pensionable pay which is at least equivalent to basic pay.

- If the rules of the scheme (or agreements) explicitly state that:

- the pension scheme requires as a minimum a total contribution of at least 9% of pensionable pay (of which at least 4% must be the employer’s contribution), or

- the pension scheme requires as a minimum a total contribution of at least 8% of pensionable pay (at least 3% of which must be the employer’s contribution) provided that pensionable pay constitutes at least 85% of earnings (the ratio of pensionable pay to earnings can be calculated as an average at scheme level), or

- the pension scheme requires as a minimum a total contribution of at least 7% of earnings (at least 3% of which must be the employer’s contribution), provided that all earnings are pensionable

then the employer can certify the pension scheme and the scheme is taken to satisfy the relevant alternative DC requirements indicated in the employer’s certification. Please note that these requirements set out a minimum contribution rate. If the scheme requires a higher rate, the employer should certify the scheme with respect to the most relevant set.

- If employers are unable to, or do not wish to, certify that their scheme meets one of the alternative DC requirements because, for example, elements of non-pensionable pay are fluctuating, they may instead be able to certify that their scheme meets the minimum requirements. They can do this if an examination of current remuneration data for all relevant jobholders reveals that their entitlement under the scheme has met the minimum requirements in practice.

- If the employer is unable to, or does not wish to, certify that the scheme meets either the minimum requirements or the alternative DC requirements, they may choose to carry out an entitlement check to establish whether the entitlement under the rules is at least equivalent to 8% of a jobholder’s qualifying earnings in the relevant pay reference period. This is an individual check for each worker, although it may be possible to group similar workers together.

- Appendix B has a flowchart (occupational schemes (full-page figure (opens in new tab)), personal schemes (full-page figure (opens in new tab))) showing the steps an employer may use to determine whether the qualifying criteria are met for a DC pension scheme with its main administration in the UK.

- If, after carrying out all the above-mentioned checks, the minimum or alternative DC requirements cannot be met, an employer may choose to change the scheme rules or agreements in one or a number of ways, including:

- increasing the rate of contributions required from the employer and/or the jobholder

- widening elements of pay included within the pension scheme definition (or definition set out in the agreements) of pensionable pay

- adopting a definition of pensionable pay, which is based on qualifying earnings and a contribution rate that meets the minimum required (ie 3% and 8% in total)

- changing the scheme rules (or agreements) to meet the DC certification criteria.

{kind=link}

{kind=link}

- When an employer is satisfied that the effect of any change(s) fulfils the relevant minimum or alternative requirements, they are then able to use it as a qualifying scheme in relation to the jobholder (provided it meets the other qualifying requirements).

- The employer should discuss any amendments to the scheme rules, and the process for making them, with the trustees, manager or providers of the pension scheme. There may be a requirement to consult with members if they are making changes to the scheme that increase member contributions. If an employer is required to consult, the consultation period is 60 days and this timing should be built into their planning for automatic enrolment.

Salary sacrifice

- Some employers make pension contribution payments by a salary sacrifice arrangement. This is a contractual agreement between the worker and the employer by which the worker agrees to forego salary in return for pension contributions by the employer (the amount sacrificed is paid into a pension scheme by the employer in respect of the worker). The operation of a salary sacrifice arrangement is separate from the automatic enrolment provisions, although an employer may run the two processes in parallel when complying with their employer duties.

- An employer may ask an eligible jobholder who must be automatically enrolled whether they want to put in place a salary sacrifice arrangement. However, active membership of a scheme cannot be dependent on whether the jobholder agrees to the arrangement. So, if the eligible jobholder declines to set up salary sacrifice, the employer must automatically enrol them in line with the automatic enrolment provisions with an alternative method of contribution deduction.

- Employers may choose to put in place a salary sacrifice arrangement before or after the jobholder’s automatic enrolment date. If they set it up before, they may choose to use postponement to give them time to put the arrangement in place. If they set it up after the automatic enrolment date, they will have to use a different method of payment for the initial pension contributions due from the automatic enrolment date.

- When communicating the option of salary sacrifice to a jobholder, the employer should take care to separate this information from the enrolment information. The employer may send salary sacrifice and enrolment information together if they wish, but must avoid giving the impression that the jobholder will only be enrolled if they agree to salary sacrifice.

- If the employer is using a DC scheme then the qualifying earnings used to meet the minimum requirement are the post-sacrifice level of salary.

Flexible benefits packages

- Similarly, some employers include their pension provision in a wider flexible benefits scheme that they provide to their workers.

- Flexible benefits schemes allow workers some freedom of choice about how they apportion their total pay and benefits. Traditionally, these schemes allow workers to choose what level of pay is committed to pension contributions alongside other benefits, such as healthcare, life assurance or cash.

- Employers can still offer this choice as long as they comply with the underlying employer duties. Therefore, for DC schemes (or DB schemes that have been permitted to qualify by meeting the DC minimum requirements) an eligible jobholder (or jobholder who has chosen to opt in) must first be enrolled into the scheme at or above the relevant minimum contribution level required to make the scheme qualifying. For a DB scheme, the eligible jobholder/ jobholder must be enrolled at or above the minimum accrual rate, or relevant cost of future accruals rate required to make the scheme qualifying. Enrolment must be able to take place at the minimum contribution level for a DC scheme (or specific type of DB scheme) (of 8% in total), or, for a DB scheme, into a scheme that meets either the test scheme standard or alternative DB requirement, even if the jobholder has not made any specific election regarding their flexible benefits options.

- Having been enrolled with effect from the automatic enrolment date, the jobholder is free to reduce or increase the level of contributions in accordance with the rules of the flexible benefits arrangement and of the scheme.

Minimum contributions entitlement for DC pension schemes

- Increases to the minimum contribution entitlements for DC pension schemes, and certain hybrid pension schemes, were phased in over the course of a number of years following the introduction of automatic enrolment.

- The minimum contributions – sometimes known as phasing – reached their current levels in April 2019. For reference and in case any backdating of contributions is required over the affected periods, the previous levels and their effective dates can be found in Table 2 below.

Table 2: How the minimum contribution entitlements increased over time

| Date effective | Employer minimum contribution | Staff contribution | Total minimum contribution |

|---|---|---|---|

| Historic rates, up until 5 April 2018 | 1% | 1% | 2% |

| 6 April 2018 to 5 April 2019 | 2% | 3% | 5% |

| 6 April 2019 onwards | 3% | 5% | 8% |

- The contribution rate for schemes using certification was also phased in over the same period. The rate will have depended on which set of certification was being used. The rates for all three sets are set out below in Tables 3-5.

Table 3: Set 1 phasing

| Transitional period | Duration | Employer minimum contribution | Total minimum contribution |

|---|---|---|---|

| 1 | Historic rates, up until 5 April 2018 | 2% | 3% |

| 2 | 6 April 2018 to 5 April 2019 | 3% | 6% |

| 6 April 2019 onwards | 4% | 9% | |

Table 4: Set 2 phasing

| Transitional period | Duration | Employer minimum contribution | Total minimum contribution |

|---|---|---|---|

| 1 | Historic rates, up until 5 April 2018 | 1% | 2% |

| 2 | 6 April 2018 to 5 April 2019 | 2% | 5% |

| 6 April 2019 onwards | 3% | 8% | |

Table 5: Set 3 phasing

| Transitional period | Duration | Employer minimum contribution | Total minimum contribution |

|---|---|---|---|

| 1 | Historic rates, up until 5 April 2018 | 1% | 2% |

| 2 | 6 April 2018 to 5 April 2019 | 2% | 5% |

| 6 April 2019 onwards | 3% | 7% | |

What next?

Once an employer is able to identify the criteria a pension scheme must meet in order to be used to fulfil their new employer duties, the next step should be to learn about the processes they will need to put in place.

For employers who know they will, or are likely to have, an automatic enrolment duty, the next step should be to read Detailed guidance no. 5 – Automatic enrolment. It contains detailed information on the automatic enrolment process, from identifying who, when and how to automatically enrol, to an employer’s ongoing responsibilities once the automatic enrolment process is complete.

It is also important for employers to understand the position of those workers who fall outside the automatic enrolment criteria, but who have a right to be enrolled into a pension scheme if they ask. Detailed guidance no. 6 – Opting in, joining and contractual enrolment explains what an employer must do if they receive a request from such a worker.

Employers should learn about the processes to put in place

Key terms

Summary of the different categories of worker

The table below is a quick reminder of the different categories of worker. These are explained in detail in Detailed guidance no. 1 – Employer duties and defining the workforce.

Table 6: Category of worker

| Category of worker | Description of worker |

|---|---|

| Worker | An employee or someone who has a contract to perform work or services personally, that is not undertaking the work as part of their own business. |

| Jobholder |

A worker who:

|

| Eligible jobholder |

A jobholder who:

|

| Non-eligible jobholder |

A jobholder who:

|

| Entitled worker |

A worker who:

|