Opting out: How to process ‘opt-outs’ from workers who want to leave a pension scheme

Automatic enrolment detailed guidance for employers no. 7

Accompanying resources

Information to workers

Summary of information requirements in a quick-reference table format

The different types of worker

Diagram of the different categories of worker and the criteria for each category

Employer duties and safeguards

At-a-glance summary of the duties and safeguards

How to save this page as a PDF

About this guidance

This guidance is aimed at professional advisers and employers with in-house pensions professionals.

It explains the opt-out process, including who can opt out, the timescales involved and the process an employer must follow when they receive an opt-out notice.

Employers who are likely to have either an automatic enrolment duty or non-eligible jobholders with a right to opt in, will need to understand the opt-out process.

In this guidance, we use ‘jobholder’ to describe both eligible jobholders (who have to be automatically enrolled) and non-eligible jobholders (who have a right to opt in).

To aid understanding of the content in this guidance, employers should be familiar with the following guidance in this series:

- Detailed guidance no. 1 – Employer duties and defining the workforce

- Detailed guidance no. 3 – Assessing the workforce

- Detailed guidance no. 5 – Automatic enrolment

- Detailed guidance no. 8 – Safeguarding individuals

‘Month’ means ‘calendar month’ throughout this guidance.

We recognise that many employers will already have pension provision for their workers, and that this will often match or exceed the minimum requirements contained in the duties. In these cases, such employers may just need to check that the minimum requirements are covered in their existing processes.

All employers must provide the regulator with certain information about how they have complied with their duties. They must submit this information within five months of their duties start date. The information can be submitted on declaration of compliance.

It will be helpful to employers to be familiar with the different categories of workers. These are explained in detail in Detailed guidance no. 1 – Employer duties and defining the workforce duties and defining the workforce or a quick reminder is available in the Key terms.

This guidance forms part of the latest version of the detailed guidance for employers (published June 2021).

Introduction

- It is compulsory for an employer to automatically enrol their eligible jobholders into an automatic enrolment scheme. It is also compulsory for an employer to arrange active membership of an automatic enrolment scheme if a jobholder opts in, or a pension scheme if an entitled worker joins.

- However, ongoing membership of the scheme is not compulsory for the jobholder. Where a jobholder has been automatically enrolled, or enrolled as a result of an opt-in request, they can choose to ‘opt out’ of a pension scheme.

- For this reason, in this guidance we use the term ‘jobholder’ to cover both an eligible jobholder and a non-eligible jobholder who decide to opt out. When reading this guidance and applying it to opting in, the following terms apply:

- for ‘automatic enrolment’ read ‘enrolment’

- for ‘automatically enrolled’ read ‘enrolled’

- for ‘automatic enrolment date’ read ‘enrolment date’.

- ‘Opt out’ has a specific meaning in pensions reform. It refers to the provision of a mechanism under the law which has the effect of undoing active membership, as if the worker had never been a member of a scheme on that occasion. It can only happen within a specific time period, known as the ‘opt-out period’. Paragraphs 16 to 30 have more information about the opt-out period.

- In addition, all workers who have become active members of a pension scheme can choose to cease membership of that scheme in accordance with the scheme rules.

- This guidance explains both the considerations and actions for an employer where a jobholder chooses to opt out or a worker chooses to cease membership. Paragraphs 16 to 49 cover opting out. Paragraphs 50 to 56 explain ceasing membership.

When the right to opt out applies

- Eligible jobholders may choose to opt out after they have been automatically enrolled.

- Non-eligible jobholders who have opted in may choose to opt out after they have been enrolled.

- Workers who have been enrolled under contractual enrolment (eg under their contract of employment) and entitled workers who have asked to join a scheme do not have the right to choose to opt out. If they want to leave the scheme, they must cease membership in accordance with the scheme rules.

When a jobholder can opt out

- Before a jobholder can choose to opt out of pension scheme membership, they must:

- have become an active member of the pension scheme under the automatic enrolment or opt-in provisions, and

- have been given the enrolment information from their employer

- The latter is important to ensure the jobholder will have been provided with sufficient information about the effect of the enrolment, so they can make an informed choice about whether to opt out.

- There are specific timescales during which jobholders can opt out of active pension scheme membership. They can only opt out during what is known as the ‘opt-out period’, which starts after active membership has been achieved. Paragraphs 16 to 30 have more information.

How a jobholder opts out

- If the jobholder wishes to opt out after being given this information, they must do so by giving an ‘opt-out notice’ (see paragraphs 31 to 40) to the employer, which is usually provided by the pension scheme.

- On receipt of the opt-out notice, the employer must take action to unravel the membership of the scheme so that the jobholder is treated as if they were never a member on that occasion. This includes giving refunds of any contributions that have been deducted. Paragraphs 41 to 49 have more information.

- An employer must keep records of any opt-outs because they will be required to re-enrol on the three-yearly re-enrolment date. Paragraphs 63 to 68 have more details.

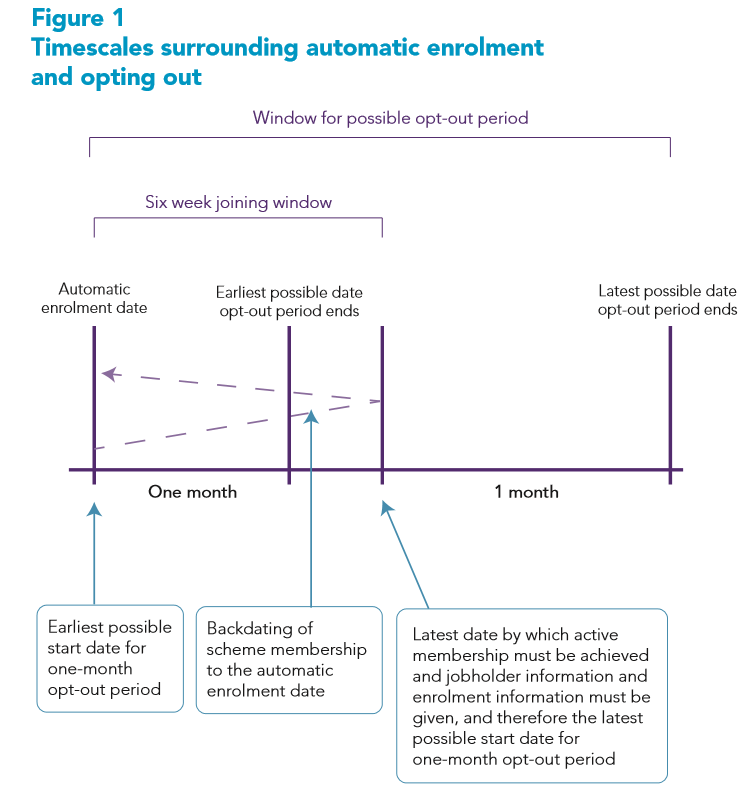

The opt-out period

- A jobholder who becomes an active member of a pension scheme under the automatic enrolment provisions has a period of time during which they can opt out. This also applies to those who become active members under the opt-in provisions. This is known as the ‘opt-out period’.

- For occupational pension schemes, the opt-out period starts from the later of the date the jobholder:

- becomes an active member with effect from the automatic enrolment date (ie the date that the administrative steps for achieving active membership are completed), or

- is given written enrolment information (see example 1)

- For personal pension schemes, the opt-out period starts from the later of when the jobholder is:

- given the terms and conditions of the agreement to become an active member (see example 2), or

- given written enrolment information

Example 1: Occupational pension scheme

Emily’s first day of employment with her employer is 7 January. She is 25 years old and her salary will be £31,000. She will be paid monthly.

Her employer knows that the first day of employment is an ‘assessment date’ and so assesses that on that date, Emily is an eligible jobholder and must be automatically enrolled.

On 7 January (the start of the joining window), her employer gives the trustees of the automatic enrolment scheme the required information about Emily. On 14 January, her employer checks with the pension scheme that active membership has been achieved. On 16 January, her employer gives Emily the required enrolment information.

Emily’s opt-out period starts from 16 January (as this is the later of the date when active membership was achieved or the enrolment information was given).

Example 2: Personal pension scheme

Tristan gave his employer an opt-in notice on 5 June. He is paid monthly in respect of the calendar month. His employer checked that the notice was valid and knows that they must enrol him from 1 July. His employer already has a group personal pension scheme that meets the automatic enrolment criteria and which they are using to fulfil their automatic enrolment duties. His employer decides to use this pension scheme for Tristan as well.

On 1 July, his employer gives the provider of the pension scheme the required information about Tristan. On the same day, they give Tristan the required enrolment information.

On 3 July, his employer checks with the provider of the pension scheme, who advises that the terms and conditions were given on 2 July.

Tristan’s opt-out period starts from 2 July (as this is the later of the date when the terms and conditions were given or the enrolment information was given).

- These steps must be completed before the end of the six week joining window (the period during which automatic enrolment must be completed). Therefore, the latest date by which the opt-out period must start is six weeks after the automatic enrolment date.

- Equally, if the employer has completed these steps by the automatic enrolment date, the earliest date the opt-out period can start is the automatic enrolment date.

- Figure 1 illustrates these prescribed timescales relative to the automatic enrolment date.

Put processes in place to deal with opt-outs

To deal quickly and efficiently with optouts, the employer should put processes in place that will enable them to:

- check the validity of opt-out notices

- notify the scheme of the opt-out

- stop the deduction and payment of contributions

- refund contributions to the jobholder

- If a jobholder wants to opt out, they have one month, from and including the first day of the opt-out period, to complete a valid opt-out notice and give it to the employer.

- Employers must not accept an invalid opt-out notice, but see paragraphs 39 to 40 for more information about invalid opt-out notices.

- An opt-out notice cannot be submitted prior to the jobholder becoming an active member.

- If an opt-out notice is given after the end of the opt-out period, the employer may take whatever action is required under the scheme rules for ceasing active membership. Paragraphs 52 to 64 have more information about ceasing active membership.

- When the employer is given a valid opt-out notice, the jobholder will be treated as if they had never been a member of the pension scheme.

- The employer must stop deducting contributions. Any contributions deducted from qualifying earnings must be refunded to the jobholder.

- Jobholders who want to leave the pension scheme after the opt-out period has expired will not be able to opt out. Instead they must cease active membership, explained in more detail in paragraphs 52 to 64.

Employers must not accept invalid opt-out notices

Entitled workers

- Entitled workers who ask to join a pension scheme do not have opt-out rights. However, if the scheme is a personal pension scheme, they do have cancellation rights under FCA (the Financial Conduct Authority) rules (note 1).

- They also have the right to cease active membership, whether they are in a personal pension scheme or an occupational pension scheme. Paragraphs 52 to 64 have more information on ceasing active membership.

Note for entitled workers

[1] Please note however that FSA Policy Statement PS11/8 amends the FCA Conduct of Business sourcebook to allow providers to mirror the opt-out process, rather than applying the cancellation period in relation to all members of an automatic enrolment scheme.

The opt-out notice

Source of opt-out notice

- In the majority of cases, jobholders may only obtain an opt-out notice from the pension scheme into which they have been automatically enrolled, and not from the employer. This is a safeguard to ensure that the jobholder’s decision to opt out is taken freely and without influence from the employer.

- A jobholder could feel pressured into opting out if they were to receive the opt-out notice from their employer, either separately or with other pension scheme information.

- Such action could, in certain cases, constitute a breach of the inducement legislation. This is explained in Detailed guidance no. 8 – Safeguarding individuals.

- Occasionally, the administration of the pension scheme is delegated to the sponsoring employer in the trust deed. In these exceptional circumstances, the jobholder can get the opt-out notice from the employer.

Valid opt-out notice

- When a jobholder gives an opt-out notice, the employer must check that it is a valid notice. This means it must contain the statutory information shown in the highlighted box after paragraph 38.

- If one notice is used to cover both opting out under the automatic enrolment legislation and ceasing membership under the scheme, the employer must ensure that all the information shown in the box on page 14 and any relevant information from the scheme regarding ceasing membership is contained within the notice. The jobholder must be able to easily identify whether they are opting out or ceasing membership.

- Whatever the format of the opt-out notice, employers must ensure that the notice meets the requirement to provide the information set out in the box for it to be valid.

- Once the employer is sure that the notice is valid, they must:

- stop deducting contributions

- let the scheme know

- issue any refunds.

Information about the jobholder

- Full name of jobholder

- National Insurance number or date of birth

- Signature or, if in electronic format, a statement confirming that the jobholder personally submitted the notice

- Date the jobholder completed the form

Statutory statements

What you need to know:

- Your employer cannot ask you or force you to opt out

- If you are asked or forced to opt out, you can tell The Pensions Regulator

- If you change your mind, you may be able to opt back in – write to your employer if you want to do this

- If you stay opted out, your employer will normally put you back into pension saving in around three years

- If you change your job, your new employer will normally put you back into pension saving straight away

- If you have another job, your other employer might also put you into pension saving, now or in the future. This notice only allows you to opt out of pension saving with the employer you name above. A separate notice must be filled out and given to any other employer you work for, if you wish to opt out of that employer’s pension saving as well.

The notice must also include statements from the jobholder to the effect that they wish to opt out of pension saving and understand that, in doing so, they will lose the right to pension contributions from the employer and may have a lower income upon retirement.

Invalid opt-out notice

- If the employer receives an invalid opt-out notice, they must tell the jobholder why the notice is invalid. They should also be aware that, in these circumstances, the one-month opt-out period is extended to six weeks.

- There are also important record-keeping requirements about the opt-out notice for both the employer and the scheme, detailed in paragraphs 63 to 68.

Opt-out notices must be submitted within the opt-out period

Refunds

- All jobholders must become active members with effect from either:

- the automatic enrolment date, in the case of eligible jobholders, or

- the enrolment date, in the case of non-eligible jobholders who choose to opt in

- Contributions must be deducted on the first occasion the jobholder is paid after this date. If they then choose to opt out, the employer must refund any contributions that have been deducted.

Employers with occupational pension schemes

- As part of getting ready for their duties start date, these employers should have considered whether to negotiate a change to the due dates on the relevant schedule with the trustees or managers of the pension scheme. This should avoid the need for the pension scheme to refund contributions to the employer. Detailed guidance no. 5 – Automatic enrolment has more information.

Employer to jobholder

- When an employer is given a valid opt-out notice, they must refund to the jobholder any contributions that have been deducted from pay (less any tax due) by the refund date, which is either:

- within one month of being given the valid opt-out notice, or

- if the payroll arrangements closed before they were given the notice, by the last day of the second applicable pay reference period following the date on which the valid opt-out notice was given. This means that the employer should pay the refund in the next available payroll run after they were given the notice.

Example of refunding contributions

A jobholder is paid on the last day of each month and the pay reference period is a calendar month. Payroll arrangements close on the 20th.

A valid opt-out notice is given on 25 May. This is too late for the refund to be included in May’s pay, or for that month’s deduction to be stopped.

The employer has until 30 June (ie the last day of the following pay reference period) to refund the contributions.

- Jobholder contributions must always be refunded by the refund date set out in paragraph 44. The employer should not wait for the pension scheme to return these contributions before making a refund to the jobholder. If necessary, they must cover the cost of the refund themselves.

Scheme to employer

- If any money has been paid over to the pension scheme, it must be refunded to the employer.

- When an employer tells a pension scheme that they have been given a valid opt-out notice, the trustees, manager or pension scheme provider must refund any jobholder and employer contributions to the employer by the refund date set out in paragraph 44. The employer will therefore need to let the pension scheme know what the refund date is in each case.

- Sometimes, an employer may have an arrangement with the pension scheme for any employer contributions to be retained to offset administrative expenses. They can continue with this arrangement if they prefer, although they may wish to seek advice on the structure of such arrangements. (Please note this applies only to employer contributions, not jobholder contributions.)

Refunds outside the opt-out period

- Jobholders who leave an occupational pension scheme after the opt-out period has ended (eg they cease active membership), may also be entitled to a refund of contributions. This will depend on when their pensionable service started and the pension scheme’s own rules.

- Pensionable service means service by the member of the scheme in any employment (to which the scheme relates), which qualifies them for pension (or other) benefits under the scheme. In our view pensionable service starts when active membership of the scheme starts for example with effect from an eligible jobholder’s automatic enrolment date, re-enrolment date or from the date that a worker is contractually enrolled into an occupational pension scheme by their employer.

Ceasing active membership

- A jobholder’s right to choose to opt out expires at the end of the opt-out period. If they want to leave the scheme after this, they can cease active membership in accordance with the scheme rules.

- Entitled workers who have asked to join a scheme do not have a right to choose to opt out. Instead, they will cease active membership in accordance with the scheme rules if they decide that they do not wish to remain in the scheme.

- A worker whom the employer has enrolled into a qualifying scheme under a contractual agreement (eg under their contract of employment) rather than under the employer duties, does not have a right to choose to opt out. If they decide that they do not wish to remain in the scheme, they must cease active membership in accordance with the scheme rules. More information about contractual agreements can be found in Detailed guidance no. 6 – Opting in, joining and contractual enrolment.

- The next paragraphs set out the benefits workers are likely to receive in the event of ceasing active membership in accordance with the scheme rules. This depends on the category of worker, length of service and the type of pension scheme of which they have been a member.

In an occupational pension scheme

- The benefits due under an occupational pension scheme will depend upon the date that pensionable service started and whether the scheme is defined benefit (DB) or defined contribution (DC). When a worker ceases active membership in accordance with the scheme rules, they can either leave their contributions invested within that scheme or take a transfer value, if:

- the pension scheme is a DC scheme and provides no other benefits other than money purchase benefits, and

- pensionable service (ie active membership) starts on or after 1 October 2015, and

- the worker has pensionable service of at least 30 days

- In practice this choice to leave their contributions invested within that scheme or take a transfer value will apply, to:

- jobholders who have been automatically enrolled on or after 1 October 2015 and cease active membership in accordance with the scheme rules after the opt-out period has expired

- workers enrolled under a contractual agreement on or after 1 October 2015 who cease active membership in accordance with the scheme rules 30 days or more after joining

- entitled workers who asked to join a scheme who have ceased active membership in accordance with the scheme rules 30 days or more after active membership of that scheme started, provided that active membership of the scheme started on or after 1 October 2015

- This choice means that workers meeting the conditions above are not entitled to a refund of contributions when they cease active membership under the scheme rules. Neither is the employer entitled to a refund of their contributions.

- Where the conditions in paragraph 55 are met, a refund of worker and employer contributions will be payable to:

- jobholders who have been automatically enrolled on or after 1 October 2015 and who opt out during the opt-out period

- workers enrolled under a contractual agreement on or after 1 October 2015 who cease active membership in accordance with the scheme rules within 30 days of the start of active membership, and the scheme rules provide for a refund of contributions

- entitled workers who asked to join a scheme and

- they have ceased active membership in accordance with the scheme rules within 30 days of the start of active membership of that scheme,

- the scheme rules provide for a refund of contributions,

- active membership scheme started on or after 1 October 2015

- If, however, the pension scheme is a DC only scheme but the pensionable service started before 1 October 2015, the benefits due will depend on the length of pensionable service. The different options are set out in Table 1.

Table 1: The benefits due in an occupational pension scheme

| Length of pensionable service | Benefit received |

|---|---|

| Less than three months | As stated in the pension scheme rules |

| More than three months but less than two years | Pension scheme rules may provide for a preserved benefit but if they do not, there is a statutory right to be offered the choice of a cash transfer sum or a contribution refund. For more information, see the notification of right to cash transfer sum or contribution refund module of our code of practice. |

| More than two years | Choice of preserved benefit or cash equivalent transfer value |

- In practice, these benefits will apply to:

- jobholders who have been automatically enrolled before 1 October 2015 and who cease active membership in accordance with the scheme rules anytime after the opt-out period has expired

- workers enrolled under a contractual agreement before 1 October 2015 who have ceased active membership in accordance with the scheme rules at any time after joining

- entitled workers who asked to join a scheme and

- they have ceased active membership in accordance with the scheme rules

- active membership of the scheme started before 1 October 2015

It does not matter if active membership ceases on or after 1 October 2015, these benefits will still apply.

- If the occupational pension scheme provides any benefits other than money purchase benefits then the different options in table 1 also apply irrespective of when pensionable service started, or the length of that service.

Employers and schemes should keep records of opt-outs

In a personal pension scheme

- Jobholders who have been automatically enrolled and cease active membership of a personal pension scheme in accordance with the scheme rules after the opt-out period has expired, can either leave their contributions invested within that scheme or take a transfer value.

- Entitled workers who have asked to join a scheme and any workers enrolled into a personal pension scheme under a contractual agreement do not have opt-out rights, but do have a 30-day cancellation period. If they change their mind and decide to cancel within this period, the pension scheme will refund any contributions paid. If they wish to leave the personal pension scheme after this period, they have the same choices as jobholders who have been automatically enrolled and who have ceased contributions after the opt-out period has expired (see paragraph 62).

Choosing to pay contributions below the minimum level

- Some jobholders, having been automatically enrolled, may decide that they wish to stay in the scheme but on a lower contribution rate than that required by legislation. This may be the case if, for example, the employer offers a flexible benefits plan with a choice of pension contribution levels.

- Such jobholders may opt out within the opt-out period, which would entitle them to a refund of any contributions deducted. As long as the rules of the scheme allow them to contribute at a lower rate, the employer would then make whatever arrangements were required for the jobholder to become an active member again at the reduced rate.

- Alternatively, the jobholder may decide not to opt out but instead, to complete whatever documentation is required by the scheme to continue membership at a lower rate. However, in this case, the jobholder would only be entitled to a refund of any contributions deducted if the scheme rules allowed it.

- If a jobholder chooses to reduce their contributions to below the statutory minimum level, the scheme will no longer be qualifying for them.

- It is important to note that the employer must not induce jobholders to reduce their contributions to below the statutory minimum level. Detailed guidance no. 8 – Safeguarding individuals has more information on inducements.

- The employer will need to keep a record of all eligible jobholders who have chosen to reduce their contributions to below the statutory minimum, as they will have to be re-enrolled into a qualifying automatic enrolment scheme on the employer’s re-enrolment date (assuming their contribution level is still below the statutory minimum at that time).

Record-keeping requirements

- It is a requirement that both employers and pension schemes keep records of opt-outs and are able to produce them, if the regulator asks to see them.

- Keeping such records also helps an employer should there be any dispute as to whether or not an individual has opted out.

For employers

- Employers must keep the original or a copy of all opt-out notices for four years. The notices can be stored in paper format or electronically.

For the pension scheme

- Trustees of occupational pension schemes and providers of personal pension schemes, must keep the following information for four years:

- The name of each jobholder who has opted out of the pension scheme

- The date when the employer notified the pension scheme that the jobholder had opted out.

And they must keep the following information for six years:

-

- The date on which any jobholder ceased active membership of the pension scheme.

- The date on which any jobholder ceased active membership of the pension scheme.

- See Detailed guidance no. 9 – Keeping records for more information about the types of records that should be kept and who should keep them.

- The regulator has previously produced guidance on the importance of good record-keeping. Although aimed at trustees and professional advisers, employers may find it useful. For further information, see our guidance on scheme member data quality.

Key terms

Table 2: Summary of the different categories of worker

| Category of worker | Description of worker |

|---|---|

| Worker | An employee or someone who has a contract to perform work or services personally, that is not undertaking the work as part of their own business. |

| Jobholder |

A worker who:

|

| Eligible jobholder |

A jobholder who:

|

| Non-eligible jobholder |

A jobholder who:

or

|

| Entitled worker |

A worker who:

|